Supply Chains:

Prepared by the Economic Division in Wellington.

On this page

Rāpopoto - Summary

- Given the ongoing risks to New Zealand’s global supply chain connections since the COVID-19 pandemic, MFAT’s network of Posts and the Trade Recovery Unit have been monitoring the operations of New Zealand’s sea and air freight connectivity, and have published reports on this since June 2020. This report provides a snapshot of how global supply chains are functioning offshore, significant international initiatives affecting supply chains, and other issues of interest to New Zealand exporters and importers.

- To provide feedback or information relevant to this report – please contact exports@mfat.net

Pūrongo - Report

Waka rererangi – air freight

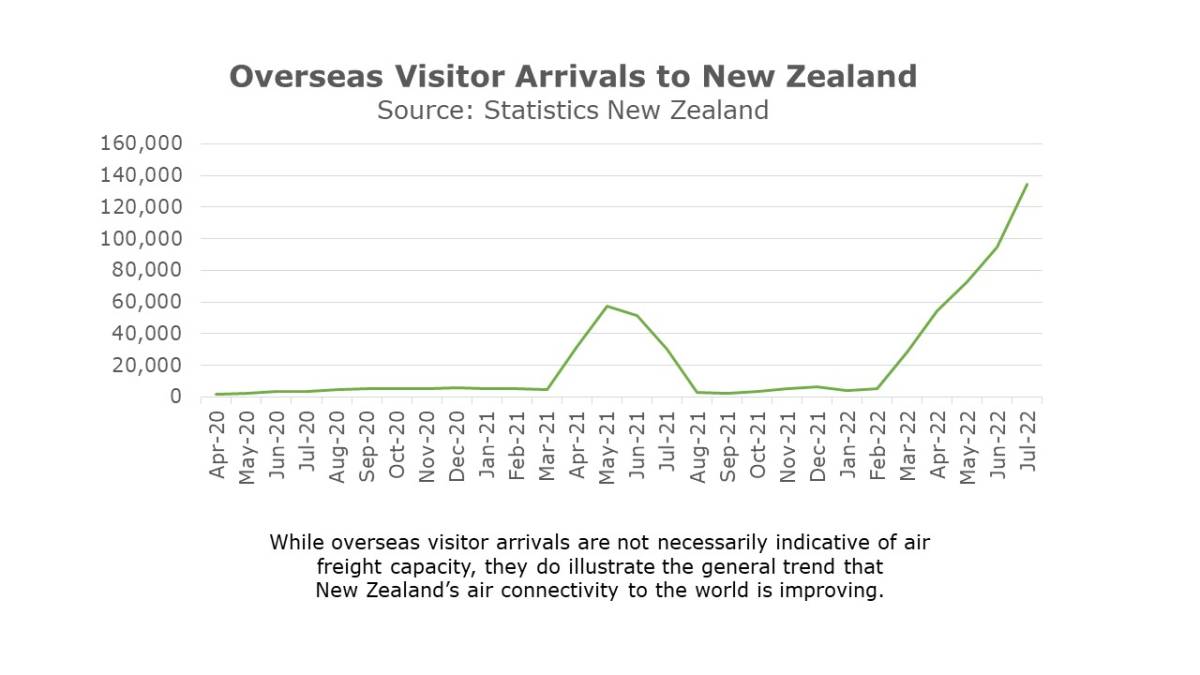

- New Zealand’s air connectivity is improving following the reopening of the border to all visa categories on 31 July. The number of seats available to and from Auckland Airport is currently around 50% of where it was in 2019, and the airport anticipates reaching about 70% by December 2022.

- Airlines are increasing the range of flights available to and from New Zealand. Air New Zealand has announced that it will resume flying from Auckland to a variety of destinations in the second half of the year, including Adelaide, Cairns, Hobart, the Sunshine Coast, Noumea, Honolulu, Houston and Chicago. Its flagship Auckland to New York route launched in September, with three round-trip flights now on offer each week. The airline plans to carry around 8000 kilograms of cargo per flight. This will primarily consist of e-commerce products, fresh flowers and seafood.

- Cargo and passenger demand is strong across some routes, including North America, South America and the Middle East. Overseas visitors to New Zealand topped 100,000 in July for the first time since the border closed March 2020. However, other routes are seeing imbalances of inbound and outbound travel/ freight. Both cargo and passenger prices remain elevated.

- New Zealand’s connectivity with South East Asia and Europe is presenting challenges. There are currently no direct flights from New Zealand to Thailand and India. Hong Kong, Shanghai and Japan were the main transit hubs for passengers and cargo to Europe pre-COVID, but these are not easily accessible under COVID-19 restrictions. Alternative hubs such as Dubai and Singapore are consequently facing increased pressure.

- Labour shortages are an ongoing pain point for the aviation industry. Auckland, Wellington and Christchurch Airports have all hosted job fairs in an effort to fill hundreds of open roles during the quarter. Emirates has had to delay plans for a Christchurch to Dubai route, and logistics company DB Schenker is only able to operate freight flights from the US to China at 50% capacity due to a lack of staff.

Mārunga moana – sea freight

- International sea freight is still experiencing some delays, congestion, and capacity constraints. However, bottlenecks in Asia are gradually easing, and demand is softening as consumer spending patterns shift from goods towards services.

- According to Flexport’s Ocean Timeliness Indicator, the time taken for containers to travel across the Transpacific Eastbound (China to the US) route has decreased from 110 days in April to 86 days in late September. Times for the Far East Westbound (China to Europe) route have likewise gone from over 120 days in April to 96 days. This is a significant improvement (though well above September 2019 levels, where travel times were under 60 days for both routes).

- Shipping prices appear to be stabilising, albeit at higher rates than before COVID. Freight forwarder Rocket Freight notes that the cost of shipping a 20-foot container from China to New Zealand has dropped from about US$12,000-$15,000 at the height of the pandemic to $5000-$6000 now. While this may indicate movement towards ‘normalisation,’ it is not the pre-COVID norm of just $800 per container.

- Global schedule reliability is also getting better. Schedule reliability refers to the probability that vessels arrive and depart on time compared to the schedule published by the carrier. New Zealand supply chains company Kotahi reports that international schedule reliability modestly increased from 35% in July 2021 to 40.5% in July 2022. But schedule reliability in New Zealand fell below 30% in July for all ports except Nelson. This was because of poor weather and staff illnesses.

- Mediterranean Shipping Company, the world’s largest container line, has announced plans to expand into air cargo.

Regional updates

United States

- Shipping congestion and delays at US ports have been somewhat alleviated this quarter. The number of ships waiting to enter San Pedro Bay (on which the Ports of Los Angeles and Long Beach sit) dropped from 19 in May to just eight by mid-September. This compares to a peak of 109 in January. As demand has dropped for shipping between Asia and the West Coast, prices have fallen from around US$20,000 last August to $4000 now.

- However, pressure on US rail networks could jeopardise progress. Containers at the Port of Los Angeles had to wait an average of 16.5 days to be picked up by train in August, which the Port attributed to labour and equipment shortages. US railroads account for about 30% of domestic cargo transport by weight (mostly food, energy, automotive products and construction materials). Disruptions could impact domestic supply of food and fuel as well as exacerbate delays at ports.

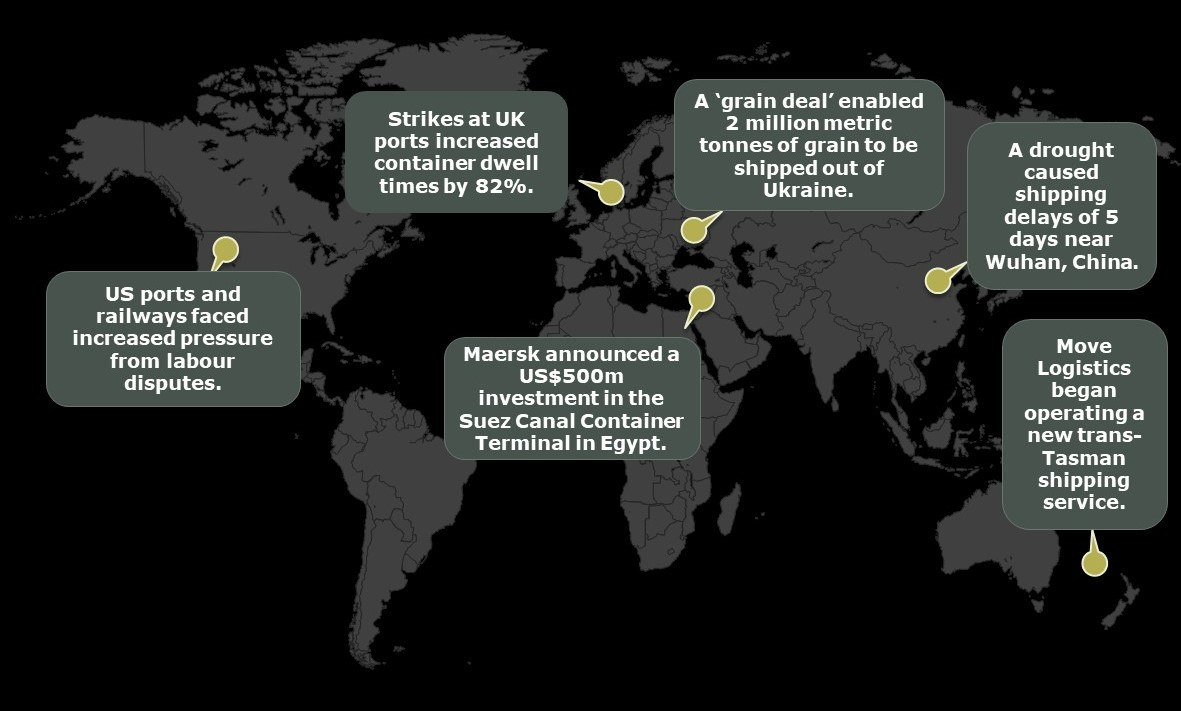

- Domestic labour disputes could also pose a risk to supply chains. Protests were held by truckers at the Port of Oakland in July over California’s independent contractor law, Assembly Bill 5 (AB5). AB5 seeks to limit the use of independent contractors, mostly by reclassifying them as employees. Port access was blocked for five days, and dwell times for containers waiting to be picked up rose from 10 to 14 days. Shipping volumes dropped by 28% overall while backlogs were cleared. Similar delays may arise elsewhere as negotiations are under way at a number of other ports/railroads over pay and working conditions.

- The US continues to face shortages of some essential goods, including infant formula and high purity aluminium.

- Four flights have transported infant formula from New Zealand to the US over the quarter.

- The US is investing in its transport infrastructure as well as the domestic production of essential goods. Rebuilding American Infrastructure with Sustainability and Equity (RAISE), a US federal programme, has awarded almost US$57 million in grant funding to improve rail capacity at ports in Nevada, Florida and Wyoming, and to develop inland ports in Utah. Along similar lines, the recently passed Creating Helpful Incentives to Produce Semiconductors (CHIPS) and Science Bill provides US$50 billion to incentivise US manufacturers to produce chips domestically.

Indonesia

- Indonesia is experiencing an outbreak of foot-and-mouth disease (FMD). Although it does not affect food safety, FMD compromises production and growth, particularly of milk. Over 500,000 animals in 25 provinces (out of 34) are affected, and there are some reports that milk production has dropped by between 60% to 90% in some areas.

- The Indonesian Government has declared a national emergency and is rolling out a vaccine programme. About 5% of the total livestock population has been vaccinated. The Ministry of Primary Industries has assessed the risk to New Zealand as low and there do not appear to be major supply chain implications at this stage.

China

- Southern China experienced a severe drought between June and August. During the peak of the drought, river-to-sea cargo transiting through the Port of Wuhan was disrupted, with ships needing to unload downstream and distribute their cargo to smaller boats. This extended shipping times by at least five days and raised costs for businesses.

- Port operations, warehousing, trucking/logistics services and airport operations are approaching pre-lockdown levels in Shanghai. The Port of Shanghai handled 4.3 million twenty-foot equivalent units in July, which was an increase of 16.8% from July 2021. Air New Zealand has also been able to sustain its six weekly cargo services (four cargo-only flights, two passenger/cargo flights) between Auckland and Shanghai over the past quarter. These are positive signs that supply chain disruptions are improving.

- The Chinese military undertook a series of joint live fire military exercises in six ‘exclusion zones’ around Taiwan from 4-7 August. This took place in the aftermath of US Speaker Nancy Pelosi visiting the island. Both sea and air freight were temporarily but not seriously affected, with approximately 900 flights experiencing disruption (including 50 cancelled flights) and ships being delayed by a few hours as they rerouted to avoid the exclusion zones. Taiwan’s Ministry of Transportation and Communications advises that airline and sailing routes have now returned to normal.

Ukraine

- Global grain supply has improved as a result of a ‘grain deal’ being signed on 22 July to facilitate agricultural exports from Ukraine and Russia through the Black Sea. Known formally as the Initiative on the Safe Transportation of Grain and Foodstuffs from Ukrainian Ports, this non-binding agreement creates safe corridors for commercial cargo ships to travel to and from Odesa, Chornomorsk and Pivdennyi for 120 days. These ports accounted for about half of Ukraine’s grain exports during the 2020-21 season.

- Despite a Russian missile strike hitting Odesa’s port just 12 hours after the deal was signed, which raised concerns about Russia’s intentions to honour the deal, two million metric tonnes of grain have been shipped out of Ukraine. Yet export volumes are still below pre-war levels of about five million metric tonnes of grain per month.

- Some commodity prices remain high due to the war. The World Food Programme estimates that the conflict has driven up the cost of staple foods in Africa by as much as 45%. On the other hand, world oil prices have returned to pre-war levels of about US$90 per barrel. Geopolitics intelligence platform Stratfor warns that supply constraints and risks remain with the ongoing conflict.

United Kingdom

- Labour disputes at UK ports have delayed sea freight. Dockworkers at the ports of Felixstowe (located northeast of London) and Liverpool participated in a series of strikes between late August and early October. The strikes took place during peak season for inventory restocking ahead of Christmas. Dwell times for containers rose by 82% in Felixstowe, and global shipping company Maersk rerouted vessels to mainland Europe.

Germany

- Water levels in the Rhine River fell to as low as 32 centimetres in August and cargo vessels were unable to sail fully loaded. For context, the Rhine covers more than 1300km of territory and carries barges from Europe’s industrial zones to the North Sea at Rotterdam. Countries rely on it to supply major industrial plants with fuels and raw materials. The official depth is now at 1.02 metres and must get to 1.5 metres before vessels can sail fully loaded again.

Australia

- Move Logistics, a New Zealand transport company, began operating a trans-Tasman shipping service in September to connect regional New Zealand ports (including Nelson, Timaru, New Plymouth and Bluff) with the east coast of Australia. This is the first New Zealand-operated service in over 20 years. Although large global shipping lines already cover the trans-Tasman route, they do not stop at smaller regional ports, and cargoes have to be trans-shipped at large ports such as Auckland. The route improves connectivity for the regions and could potentially offer faster, cheaper and more efficient shipping options.

- Maersk is experiencing delays on trans-Tasman routes due to operational challenges in New Zealand, including labour issues and poor weather. It does not expect improvements until early November.

Fiji

- McDonald’s ran out of beef patties in Fiji due to shipping delays in July. This followed a chicken nugget shortage earlier in the year, leaving customers to dine on Filet-o-Fish burgers.

Vanuatu

- The Pacific Islands Forum Economic Ministers Meeting was held from 11-12 August in Port Vila. A study was presented on the impacts of COVID-related supply chain disruption on the Pacific, which found that charter rates for container vessels servicing the region are growing by more than 300% per year. As 90% of goods are transported by ship to and from the Pacific, this places a considerable cost burden on supply chains.

Egypt

- Maersk has announced a US$500 million investment in the Suez Canal Container Terminal. It will be operating a new 1km container berth, which will increase the port’s capacity and reduce risks of congestion.

Supply chain resilience initiatives

- A meeting of Trade Ministers from fourteen regional economies took place in Los Angeles on 8-9 September on the US-initiated Indo-Pacific Economic Framework for Prosperity (IPEF). A Ministerial Statement on the supply chains pillar (one of the four pillars of IPEF) was released, which set out six intentions: establishing criteria for critical sectors and goods, increasing resiliency and investment in critical sectors and goods, establishing an information-sharing and crisis response mechanism, strengthening supply chain logistics, enhancing the role of workers, and improving supply chain transparency. Formal negotiations on the four pillars of IPEF will now commence.

- The European Commission has proposed a Single Market Emergency Instrument to prevent supply chain disruption during future crises. It includes measures to ensure the free movement of goods, services and people within the EU’s Single Market as well as the availability of essential goods and services in emergencies.

- A number of countries have entered into a Minerals Security Partnership to secure the supply of critical minerals for clean energy and other technologies, e.g. lithium, nickel and cobalt. Countries involved include Canada, the US, Australia, Finland, France, Germany, Japan, South Korea, Sweden and the UK.

More reports

View full list of market reports.

If you would like to request a topic for reporting please email exports@mfat.net

Sign up for email alerts

To get email alerts when new reports are published, go to our subscription page(external link).

Disclaimer

This information released in this report aligns with the provisions of the Official Information Act 1982. The opinions and analysis expressed in this report are the author’s own and do not necessarily reflect the views or official policy position of the New Zealand Government. The Ministry of Foreign Affairs and Trade and the New Zealand Government take no responsibility for the accuracy of this report.