Supply Chains, Manufacturing (excludes F&B):

On this page

Summary

- China’s “Made in China 2025” (MIC 2025) initiative has accelerated the transformation of China’s manufacturing base from low-cost, assembly-driven production to technology-intensive, high-value industries. China now accounts for around 30% of global manufacturing output. The initiative has reshaped global markets, with China now a leader in sectors such as electric vehicles, battery systems, solar panels, high-speed rail, and factory automation. Scale, vertical integration, and an innovative chain linking research to production have lowered costs and accelerated global adoption.

- China continues to pursue development in other areas such as advanced semiconductors and aircraft engines. The initiative has also created new challenges and impacts for global markets, while adding to pressure on small and medium-sized enterprises.

- Looking ahead, China’s next Five-Year Plan (2026-2030) is doubling down on dominating advanced manufacturing. The next phase of industrial policy emphasises artificial intelligence, advanced computing, smart and green manufacturing, and deeper localisation of strategic technologies.

Report

MIC 2025 was launched in 2015 as a foundational strategy to support China’s ambition of becoming a global manufacturing leader. The initiative aimed to shift the country’s industrial base from low-cost, assembly-driven production toward technology-intensive, high-value sectors. At its core, the strategy sought to strengthen domestic capabilities, reduce reliance on foreign technology, and position Chinese firms as globally competitive players.

The plan identified ten priority sectors considered critical for industrial upgrading and long-term resilience. These included information and communication technology, robotics, aerospace, maritime engineering, advanced rail systems, new energy vehicles, power equipment, agricultural machinery, new materials, and biopharmaceuticals and medical devices. These sectors were selected for their strategic importance in driving innovation, supporting economic modernisation, and securing supply chain security.

To achieve these objectives, MIC 2025 set clear goals: increase domestic content in key industries, reduce foreign technology dependence, build internationally competitive businesses, and promote greener and more digitised manufacturing practices.

A decade in three acts

The first phase of MIC 2025 (2015–2018) focused on laying the groundwork for industrial upgrading through investments in logistics networks, modernised ports, and renewable-powered industrial parks. Mechanisms were introduced to accelerate the transfer of research into production, with companies positioned as innovation drivers supported by targeted funding and procurement policies. Shenzhen’s high-tech ecosystem exemplified this approach, enabling firms like DJI to scale rapidly and achieve global leadership in drones and service robotics.

The second phase (2018–2020) was shaped by external pressures as trade and foreign technology restrictions exposed vulnerabilities in semiconductors and aerospace. These challenges triggered a push from China to localise equipment and materials, though progress was uneven. Advanced areas such as lithography and metrology remained difficult to master. In aerospace, COMAC’s C919 passenger jet entered commercial service after years of development delays but still relies on foreign-made engines and key componentry.

The third phase (2020–2025) delivered milestones in sectors where China had scale and upstream control. Electric vehicles, solar panels, and industrial robotics became areas of global leadership, reshaping cost structures and accelerating adoption worldwide.

Notable sector outcomes

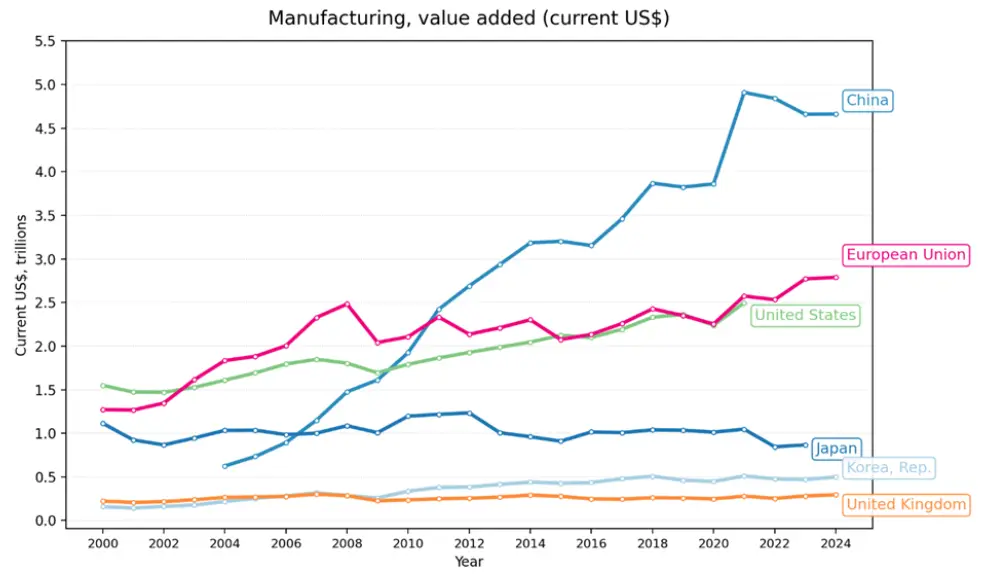

By most measures, MIC 2025 has significantly advanced China’s industrial capabilities and reduced its reliance on foreign supply chains. Ten years ago, many sectors were highly vulnerable to external disruptions. China is now more resilient, having shored up domestic production and fostered competitive firms in strategic industries. While this transformation began before MIC 2025 was introduced, the policy’s launch in 2015 set clearer goals and plans to achieve these outcomes and coincided with a notable acceleration in growth. In 2024, China’s manufacturing output exceeded US$4.6 trillion (NZ$7.9 trillion), nearly 60% higher than the United States, compared to US$3.2 trillion in 2015. China now accounts for around 30% of global manufacturing output.

Source: World Bank Data (external link)

Both Chinese and international analysts indicate that China has made substantial progress toward the goals set for the ten priority sectors, although full self-sufficiency has not been achieved in all areas. Sector performance is outlined in Annex One, but several examples illustrate the scale of change.

One of the clearest examples has been the electric vehicle industry. China is both the largest market and producer of EVs, with BYD surpassing Tesla in pure-electric deliveries after expanding from a negligible export base in 2018 to nearly one million deliveries abroad in 2025. The company also cemented its position as the world’s leading EV producer in 2025, delivering around 2.25 million battery‑electric vehicles, ahead of Tesla’s 1.64 million. BYD’s company’s strategy combines vertical integration of batteries and power electronics with frequent product updates, competitive pricing and fast charging technology, enabling rapid expansion across Asia and Europe. At the same time, CATL has consolidated its position as the backbone of the battery industry, holding nearly 38% of global market share in 2024 and supplying major international brands such as Tesla, BMW, and Volkswagen. CATL’s scale and cost efficiencies have allowed it to remain profitable despite falling average prices of batteries.

China’s car manufacturing industry more broadly benefitted from the establishment of Tesla’s giga factory in Shanghai, which opened in 2019. Meeting Tesla’s supplier requirements has forced local firms to lift production standards, which in turn elevated quality across the entire automotive supply chain. The improved components (such as windscreens) quickly became available to domestic automakers as well, acting as a major catalyst for developing China’s own car industry. This evolution underscores China’s transition from refining foreign innovation towards developing its own capabilities and exporting them abroad. Some analysts believe that a similar pattern could emerge in food production, where rising domestic food quality reduces the premium from imported food. Early signs are already evident in Chinese restaurants, where local brands are increasingly competing with imported products – a trend with significant implications for exporting countries like New Zealand.

Rail transport is another prime example. China now operates the world’s largest high-speed rail network, with more than 45,000 kilometres in service, more than the rest of the world combined. Meanwhile, China continues to make progress in developing next-generation trains, including the CR450 bullet train prototype engineered for speeds of up to 400 km/h.

In manufacturing automation, China is now the world’s largest market for industrial robots, installing about 295,000 units in 2024, roughly 54% of all robots put into operation globally. For the first time, domestic robot manufacturers captured a majority share of the Chinese market. This has been spurred on by the rapid adoption of industrial robots across a wide range of sectors. China’s rapid automation push also helps soften the impact of its aging population and shrinking labour force.

Outcomes are also evident in information technology and artificial intelligence. Despite facing external sanctions since 2019, Huawei emerged as a national champion in this sector. The company reported revenues of CNY860 billion (NZ$211 billion) in 2024, a 22% increase year-on-year. Growth was driven by a rebound in domestic smartphone sales using in-house chipsets, as well as expansion in cloud services, AI applications, and smart-car solutions.

China is the world’s largest buyer of semiconductor equipment and is increasing domestic production capacity through new plants. However, there is still reliance on foreign supply of advanced technologies such as extreme ultraviolet lithography and leading-edge nodes. That may be changing, China is pursuing its own EUV system, with a Shenzhen lab reportedly assembling a prototype. The machine can generate EUV light but has yet to produce chips. Current estimates suggest that China can produce about 20% of its semiconductor needs domestically, with ambitions to reach 50–60% by 2030.

From blueprint to reality

The implementation of MIC 2025 relied on several core strategies designed to strengthen industrial capacity and accelerate technological adoption. One of the most influential approaches was scale and vertical integration. By linking raw materials, equipment, and finished products within unified supply chains, China was able to reduce costs and increase production efficiency. This model was particularly effective in sectors such as solar panels, batteries, and electric vehicles, where large-scale operations helped reset global cost curves and speed up market penetration.

Another key step was strengthening the innovation chain. This initiative connected research institutions, engineering teams, and manufacturing facilities to shorten the time between scientific discovery and commercial application. This chain was fostered by many levels of government schemes and subsidies which provided an abundance of resources and incentives. The innovation chain played a critical role in areas such as robotics, electric vehicle technology, and power equipment, enabling faster translation of research into market-ready products.

Financial support and early purchasing commitments from state-owned enterprises also contributed to MIC 2025 success. These mechanisms reduced risk for emerging industries and allowed production to scale ahead of market demand. By combining these strategies, MIC 2025 created an environment where firms were incentivised to innovate and expand quickly, with a view to compete not just domestically but also globally.

Challenges along the way

Despite notable outcomes, the implementation of MIC 2025 faced several constraints. Progress across firms has been uneven. Large enterprises were able to adopt advanced technologies quickly, while smaller businesses struggled with the high costs of automation and digital upgrades. For example, large automakers such as BYD or cross-sector giants like Xiaomi and Huawei, rapidly integrated robotics and smart manufacturing systems, whereas smaller suppliers found these investments prohibitive. This disparity has slowed the diffusion of innovation across the broader sectors.

Overcapacity has emerged as another outcome, with solar panels being an example. The ecosystem promoted by MIC 2025 led to situations where production significantly exceeded demand, leading to price reductions and pressure on manufacturers’ margins. These cycles have had an impact on domestic and global markets raising concerns about sustainability and profitability in highly scaled industries. More recently in response to domestic concerns, the Chinese Government has launched an “anti-involution” campaign to try to address some of the negative effects of this ‘race to the bottom’ or zero-sum intra-company competition.

What comes next: MIC 2.0?

Although the MIC 2025 label has become less prominent in official discourse since 2018, the underlying policy direction remains clear. Its objectives have been absorbed into broader frameworks such as the 14th Five-Year Plan and the ‘dual circulation’ strategy, as well as targeted initiatives like ‘AI + Manufacturing’ and intelligent factory programs.

China’s 2026-2030 Five-Year Plan has signalled a focus on using AI and other advanced technologies to upgrade traditional industries, achieving greater independence in science and technology and expanding China’s innovation capacity.

More reports

View full list of market reports(external link)

If you would like to request a topic for reporting please email exports@mfat.govt.nz

Sign up for email alerts

To get email alerts when new reports are published, go to our subscription page(external link)

Learn more about exporting to this market

New Zealand Trade & Enterprise’s comprehensive market guides(external link) export regulations, business culture, market-entry strategies and more.

Disclaimer

This information released in this report aligns with the provisions of the Official Information Act 1982. The opinions and analysis expressed in this report are the author’s own and do not necessarily reflect the views or official policy position of the New Zealand Government. The Ministry of Foreign Affairs and Trade and the New Zealand Government take no responsibility for the accuracy of this report.

Copyright

Crown copyright ©. Website copyright statement is licensed under the Creative Commons Attribution 4.0 International licence(external link). In essence, you are free to copy, distribute and adapt the work, as long as you attribute the work to the Crown and abide by the other licence terms.