Supply Chains, Food and Beverage:

On this page

Summary

- A rapidly growing middle class and increasing disposable incomes are driving change in dietary and food expenditure in Viet Nam. Vietnamese consumers are becoming more health-conscious and willing to pay more for imported food products that they view as better quality and produced according to higher safety standards. Retail sales of food and beverages in Viet Nam reached USD51 billion in 2020, after growing 10 percent annually in the years 2016-2020.

- As Vietnamese consumers become more affluent, non-price factors are becoming more important in decision-making. Food safety is often ranked highest when choosing food and beverage products, followed by quality and price. Perceptions of New Zealand products in Viet Nam tend to be positive but awareness is limited, and there is a good opportunity to raise New Zealand’s profile as a provider of safe and premium quality food and beverage products.

- Rapid expansion of modern convenience stores and supermarkets across Viet Nam, as well as rapid uptake of e-commerce, presents opportunities for New Zealand exporters, a significant growth opportunity for New Zealand products, and a valuable product-to-market mechanism.

- Imported fruits are increasingly being used as gifts during special Vietnamese holidays, and New Zealand wine exports to Viet Nam under the ASEAN Australia New Zealand FTA (AANZFTA) currently enjoy a tariff advantage compared to European or South American wine imports. Fresh fruit and vegetables, as well as some animal products, can still face barriers in the form of importing requirements which can take time to overcome.

Report

- Viet Nam’s middle class is expected to grow to 50 percent of the population by 2035 as more than 36 million consumers are expected to enter the middle class in the next decade. Continuing urbanisation will see more than 40 percent of Viet Nam’s over 100 million population live in the major cities of Ha Noi, Ho Chi Minh City, and Da Nang, as well as emerging secondary cities including Can Tho and Hai Phong.1

- Prior to the pandemic, Viet Nam’s economy has been averaging around 5.5 percent GDP growth per year since 1990, second only to China in terms of fastest rates of per capita growth over the same period. While COVID-19 and global economic uncertainty will slow growth, Viet Nam retains strong growth aspirations and aims to be a middle-income country by 2035. This puts Viet Nam today on par with Malaysia’s economic development status in 2001, and Brazil’s in 2014.2

- Income growth and demographic change are also bringing major shifts in dietary and food expenditure patterns. Among Viet Nam’s urban population the share of food expenditure on rice has fallen from 25 percent in 2002 to less than 10 percent in 20163. At the same time, as incomes increase, demand for imported products has increased. Consumer spending on imported food and beverages has grown steadily and in 2020 reached USD51 billion on food and beverage alone. Of that, 30 percent was spent on fresh food, 14 percent on packaged food, 3.5 percent on non-alcoholic drinks, and 3 percent on alcoholic drinks.4

The Vietnamese retail market

- Traditional trade channels, such as small shops owned by families and/or run on an individual basis, and kerb-side markets, still dominate the retail food sector with upwards of 75 percent of grocery trade. However, this dynamic is also rapidly changing. Viet Nam’s two largest supermarket retailer brands built more than 100 new convenience

stores in April 2022 alone, and have plans to construct between five to ten major supermarkets annually through to 2028. - This rapid growth in modern retail presents an opportunity for New Zealand exporters. Retail spending in e-commerce is also growing rapidly, driven by widespread use of smart phones and high levels of broadband penetration.

Consumer preferences

- Product attributes influencing Vietnamese consumers tend to be quality, especially with products that are perceived to meet high food safety standards or have perceived health and wellness benefits, and products made with fresh, natural, and/or organic ingredients. 5 6 Among Viet Nam’s middle class, these factors are often ranked ahead of other considerations such as price.

New Zealand’s food and beverage exports

- New Zealand’s exports to Viet Nam are currently dominated by food and beverage products. This includes dairy, fresh fruit and vegetables, meat and wine. Of this, dairy is the most valuable export at NZD408 million to December 2021. Food and beverage exports to Viet Nam have stood up well despite COVID-19 supply chain disruptions and increased logistics costs, growing by 12 percent per year between 2015 and 2020. As hospitality and tourism services rebound following the COVID-19 pandemic growth, especially in this sector, is expected to be

relatively rapid. - The last two years have seen particular growth in exports of casein (up 9 percent since 2020 to NZD6.6 million), fruit and nuts (up 13 percent), and chocolate (up 88 percent).

- While there still remains strong growth opportunity for New Zealand food and beverage exports, Viet Nam is a crowded market with strong competition from domestic producers in some sectors, and from other countries looking to take advantage of Viet Nam’s rapidly growing market.

- Trade with Viet Nam is also not always easy. New Zealand has secured market access to Viet Nam for exports of fresh cherries, passionfruit, persimmon, kiwifruit and kiwi berries, apricots, apples, and blueberries. Market access for strawberries is expected to be granted in 2022. Securing market access for new products can be complex and time-consuming. Exporters also need to ensure that Vietnamese import health standards are met, as well as ensuring cold-storage and hygiene standards from the exporting house throughout the transportation chain to retail shelves.

The Vietnamese dairy market

- While the market for dairy products in Viet Nam has grown considerably in recent years, per capita consumption is still low compared to other countries in the region. There is, however, also a strong correlation between dairy consumption and income level so as Viet Nam’s middle and high income groups grow and become more health-conscious, dairy consumption is expected to increase.7

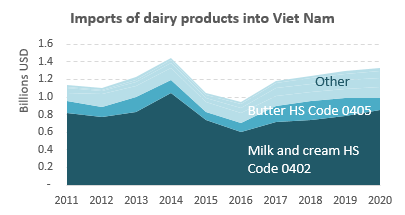

- Approximately USD5.9 billion was spent on dairy products in 2020 (8.3 percent growth year on year). Over threequarters of the total market is made up of liquid and powder milk, while yogurt, cheese, butter, and other dairy products each make up less than 15 percent of the market.8

- Viet Nam’s domestic dairy industry has grown to meet increasing demand, but the country remains highly dependent on imports. Local dairy production (from 405,000 cows) produced nearly 1.2 million tons of fresh milk in 2020, but this only provided 60 percent of production inputs.9 Viet Nam spends around USD1.2 billion annually importing dairy products to provide the balance of inputs for production, and to meet local demand.

- New Zealand is by far the largest exporter of dairy products to Viet Nam, dominating many product groups including liquid milk, butter, and infant formula. New Zealand’s products are supported by a reputation for food safety and quality and consistently account for approximately 40 percent of total imports. In the last two years particular growth has been seen in casein exports (9 percent growth). The US is the second largest exporter. Australia and the Netherlands are more minor exporters, securing between three and 11 percent of market share.

The wine market: potential for growth

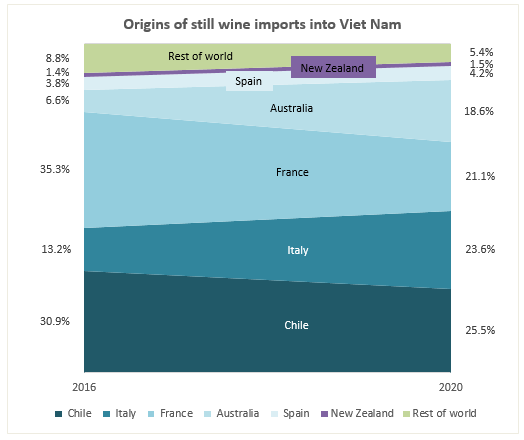

- As consumer tastes change and the middle class gets larger, imported wine is increasingly competing with (largely domestically produced) beer for share of the alcohol market. In 2020 Vietnamese consumers purchased 15.3 million litres of alcohol.10 The largest suppliers of wine to Viet Nam, in order of export volume, are Chile, Italy, France, Australia, Spain and New Zealand.

- In 2020, wine revenue in Viet Nam amounted to USD225 million. Demand for wine is dominated by young adults living in the major cities in Viet Nam, where wine is seen as a luxury good and often given as a gift during special events or festivals, for instance around the New Year and Tet Lunar New Year holidays. Wine sales took a dip between 2020 and 2021 due to prolonged lockdowns, but are expected to grow 4.3 percent annually during the 2022-2025 period as the hospitality industry and tourism sectors recover from the impact of the pandemic.11

- Red wine dominates wine sales in Viet Nam, accounting for approximately 76 percent of total wine consumed in 2020, followed by white wine at 18 percent.12 Strong competition is emerging in the wine market in Viet Nam, especially from Chile (which is also a member of CPTPP), France and Italy (which often receive preferential tariff treatment under the European Union-Viet Nam Free Trade Agreement – the EVFTA), and Australia (which is a member of CPTPP and AANZFTA). Italian and Australian wines have become more popular in recent years, increasing from 20 percent of import value in 2016 to 42 percent in 2020.

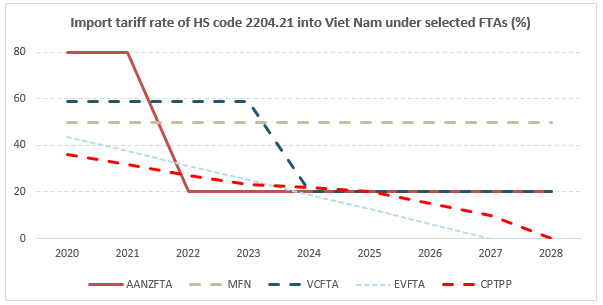

- New Zealand is currently the 6th largest supplier of wine to Viet Nam, and market share remained modest throughout 2016-2020, accounting for approximately 1.5 percent of import value in 2020. Until recently the import tariff of wine into Viet Nam under AANZFTA was 80 percent, which is higher than the MFN rate and higher than the rate offered under the Vietnam-Chile FTA or the EU-Vietnam FTA (EVFTA). See the Figure above.

- However, 2022 may bring an opportunity for New Zealand wine exports to Viet Nam. From 1 January 2022 the tariff rate offered under AANZFTA decreased to 20 percent, making it the lowest tariff rate among Viet Nam’s large wine suppliers and lower than the tariffs encountered by competitors from Europe or Chile. Wine exporters from New Zealand exporting under AANZFTA are expected to have this advantage until 2024 when the EVFTA rate will drop to 18.75 percent. Both CPTPP and EVFTA are expected to reach 0 percent by 2028.

The fruit market: blossoming potential

- Vietnamese consumers are also spending more and more on imported fruit and vegetables. According to the Ministry of Agriculture and Rural Development, in 2019 Viet Nam spent USD1.775 billion on imported fruits and vegetables. With increasing disposable incomes Vietnamese consumers are willing to pay more for imported fruit and vegetables that they view as meeting higher quality and safety standards.

- Concern about pesticide residue on domestically produced fruits and vegetables is a strong factor behind purchasing decisions. This creates opportunities for New Zealand horticultural products to be well-positioned as ‘premium products’ underpinned by strong food safety and hygiene standards. Imported fruits are frequently purchased as gifts or during special holidays such as the Tet Lunar New Year.

- Apricots, cherries, peaches, plums and sloes have also been increasing in sales, to NZD10.02 million in 2020. Nearly 90 percent of kiwifruit imported into Viet Nam are from New Zealand.

- Research commissioned in 2022 by New Zealand Trade and Enterprise (NZTE) indicated that Vietnamese consumers had high opinion, but low awareness, of New Zealand apples. In the five years to 2020, New Zealand exports of fruits and nuts to Viet Nam grew 39 percent annually to NZD130.2 million (of which apples accounted for NZD92 million).13 New Zealand apples still only account for 14 percent market share in Viet Nam, indicating there is room to grow market share.

- New Zealand exports to Viet Nam of fresh cherries, passionfruit, persimmon, kiwifruit and kiwi berries, apricot, apples, and blueberries all currently enjoy 0 percent import tariffs under AANZFTA.

References

- The new faces of the Vietnamese consumer | McKinsey(external link)

- Viet Nam 2035: Towards Prosperity, Creativity, Equity, and Democracy(external link)

- Result of the Vietnam household living standards survey 2018(external link)

- Viet Nam food and beverages retail sales by category(external link)

- Viet Nam Consumer Survey, 2020. Deloitte(external link)

- Retail Sector Market Entry Guide, 2018. Dezen Shira & Associates(external link)

- The 2020 EU Food and Beverage Market Entry Handbook for Viet Nam(external link)

- Euromonitor International(external link)

- Nganh sua thich ung bien nguy thanh co(external link)

- Trading wine in Viet Nam - Why and how to proceed(external link)

- Wine in Viet Nam(external link)

- Rising disposable incomes augment wine consumption in Viet Nam(external link)

- Stats New Zealand(external link)

More reports

View full list of market reports.

If you would like to request a topic for reporting please email exports@mfat.net

Sign up for email alerts

To get email alerts when new reports are published, go to our subscription page(external link).

Disclaimer

This information released in this report aligns with the provisions of the Official Information Act 1982. The opinions and analysis expressed in this report are the author’s own and do not necessarily reflect the views or official policy position of the New Zealand Government.

The Ministry of Foreign Affairs and Trade and the New Zealand Government take no responsibility for the accuracy of this report.