Food and Beverage, Primary Products, Sanctions:

On this page

Prepared by the Economic Division in Wellington

Summary

Limited bilateral trade but exposure to indirect economic fallout likely

- The Russian invasion of Ukraine and resulting economic sanctions imposed by a large number of countries, including New Zealand, on Russia are raising the prospect of disruption to global financial and commodity markets.

- New Zealand’s distance from the military action between Russia and Ukraine combined with limited bilateral trading relationships (Russia is our 27th largest export partner) will help insulate New Zealand from the direct economic effects of the invasion. In particular, the global conditions and supporting factors that led to major falls in dairy commodity markets during the annexation of Crimea in 2014, are not currently present. Exports were only $293 million in the year to June 2021 (half of which was butter) and could potentially be diverted elsewhere. New Zealand imports from Russia, which are mostly crude oil, have dropped to close to zero in recent months.

- The most significant impacts on New Zealand of the invasion will be indirect, primarily through higher fuel and commodity prices, financial market volatility, and the potential drag on global economic activity. The Russian action towards Ukraine is already creating significant anxiety and testing global financial and commodity markets. The price of a wide range of globally traded commodities, particularly oil and wheat, have already risen and are likely to increase further. The flow on financial effects could affect the value of the New Zealand dollar and raise the cost of some imported goods (particularly fuel), placing additional pressure on already high domestic inflation.

- For many of our key trading partners, particularly in Europe, the impact will be far more significant. To the extent that an extended invasion weighs on global economic growth, this could potentially affect the medium term prospects for New Zealand.

Report

The Russian invasion threatens to have significant global economic consequences

Over the past few weeks, tensions have flared in Eastern Europe where Russia has amassed tens of thousands of troops along the Ukraine border. On 24 February, Russian military forces began to invade Ukraine.

The United States (US), European Union (EU), United Kingdom (UK) and a range of other countries, including Australia and New Zealand, have implemented a range of economic sanctions and other measures against Russia in response to the invasion. Severe economic sanctions have already been imposed by the US, EU and others, including a targeted exclusion of Russia from the SWIFT interbank payment system used to make cross-border transfers as well as restrictions on the Russian central bank. This will make any bilateral trade with Russia highly challenging. These measures form part of a broader package of sanctions focused on finance, energy, and technology. Given how quickly sanctions continue to evolve, this note does not attempt to capture them all.

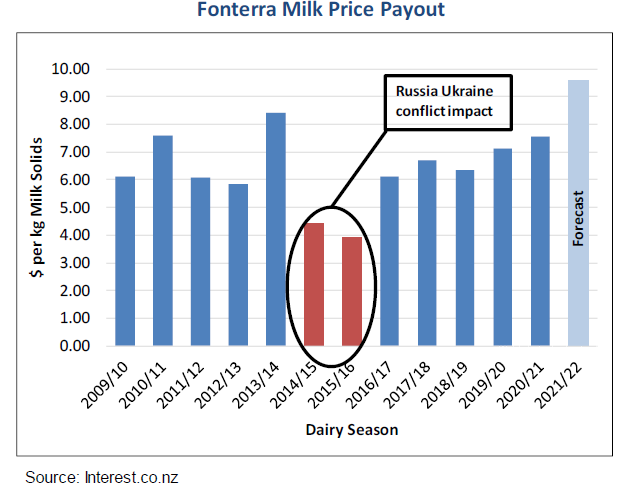

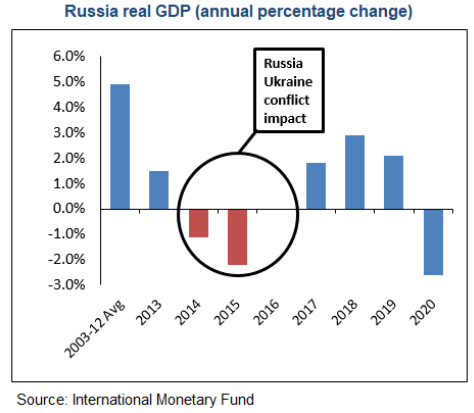

The economic impact was significant last time for key New Zealand export sectors

In March 2014 the annexation of Crimea by Russia caused significant volatility in international financial markets, with major negative impacts for key sectors of the New Zealand economy.

Dairy prices fell by more than 40% over the course of the year following Russia’s decision to ban EU agriculture exports. The EU was (and remains) the world’s largest dairy exporter, and at the time Russia was its largest market destination. This saw global dairy markets flooded with unsold product that contributed to a supply glut. (Demand from China had also eased significantly around that time).

The consequent collapse in dairy commodity prices then filtered through to New Zealand farmers with the farm-gate pay-out collapsing over the course of the following two-seasons, causing financial strain across the sector that took years to recover from.

New Zealand is less directly exposed this time

Despite similarities between the situation then and now, we do not expect to see a repeat of the financial impacts of 2014 on New Zealand’s largest export industry in the coming months.

Global dairy markets are currently in a very different position compared to 2014. EU dairy exports to Russia have collapsed following the previous round of sanctions, so the amount of diverted surplus dairy commodities on to the market will not occur to the same extent this time around.

Critically, the 2014 annexation took place at a time when global dairy production was ramping up following good weather and when European production caps were being lifted. It also occurred at a time when demand out of China was slowing. The combination of these two factors drove dairy commodity prices dramatically lower.

However the current dynamics of supply and demand for global dairy markets is very different. Global dairy supply is currently very tight. Poor weather in New Zealand has weakened production, with the season now 3.2% below the previous year. Similarly a combination of bad weather, high feed, and other key input costs such as fertilizer and fuel is constraining production in other key exporting countries such as the EU and US.

This is occurring at a time when demand, particularly out of China, is proving highly resilient (even in the face of exceptionally high dairy prices). Prices on the Global Dairy Trade Auction are currently 28% higher than a year ago, nearly 38% higher than their five year average, and at their highest level since 2014.

Nevertheless there will be some impacts should New Zealand’s dairy trade need to divert to other markets. Total dairy exports to Russia were $168.9 million for the year ending June 2021. Of this total, butter represented $147.9 million, comprising 5.5% of New Zealand’s total for this commodity - Russia was New Zealand’s 4th largest butter destination in 2021.

Looking beyond dairy markets, any sanctions on Russia itself are unlikely to have a major impact on New Zealand’s other big export sectors either, although it is likely to have more significant economic consequences for a number of smaller exporters. New Zealand’s exports to Russia have recovered since their crash in the aftermath of the tensions back in 2014, but it remains relatively insignificant as an NZ export partner.

Russia was New Zealand’s 27th largest export trading partner in the year ending June 2021, with goods exports totalling $293 million (0.5% of New Zealand’s total). Beyond dairy, the only export commodities of any significance were apples ($26.7 million), seafood ($22.4 million), wine ($15.2 million) and medical equipment ($15.2 million).

Prior to 2021, almost all imports from Russia were crude oil (well over 90%) and Russia was a moderately important source of crude oil imports (16% of New Zealand’s crude imports in 2020). The planned closure of the Marsden Point oil refinery in April will mean that New Zealand will be switching to refined petroleum products from alternative markets anyway, of which currently Korea and Singapore are currently our largest. The last significant crude oil shipment from Russia was in January 2021.

Trade with Ukraine is modest, with exports totalling $17.0m (mainly seafood and dairy) and imports of $25.4m (mainly sunflower seed oil and tobacco).

For the New Zealand seafood sector Russian and Ukrainian crews are a critical labour input for the deep sea trawler vessels operated by a number of New Zealand companies. Typically there are around 500 Russian / Ukrainian crew operating on these vessels at any one time, generally on six month rotational shifts.

Nevertheless, there could be significant indirect flow on effects for New Zealand

Although the low level of bilateral trade exposure means the direct impacts will be quite limited, this will not completely shelter New Zealand from the global market and economic pressures likely to emerge from the invasion.

While the extent of both military action and sanctions are mostly unknowns for now, they could have a serious impact on the world economy.

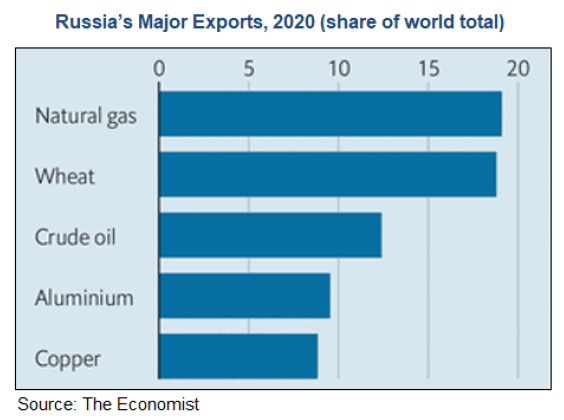

The potential for disruption stems from Russia’s importance in key global commodity markets. Russia is the world’s largest exporter of natural gas, and the second-largest exporter of oil. It supplies nearly a tenth of the world’s aluminium and copper, and produces a range of other metals, including 43% of the world’s palladium, a component of catalytic converters. It is also the world’s largest exporter of wheat.

Flows of these vital raw materials are likely to be disrupted as the situation escalates, or the payments infrastructure needed to facilitate them is hit by Western sanctions. Russia could itself decide to halt some exports (most likely gas flows to Europe) as a potential counter measure to Western sanctions.

The largest economic impact on New Zealand of the invasion would therefore be mainly indirect, through higher import fuel and commodity prices, instability of financial markets, and the impact on global economic activity. Russian action in Ukraine is already creating significant anxiety, which is testing global financial and commodity markets. The price of a wide range of globally traded commodities, particularly oil and wheat, have already risen and are likely to increase further. The flow on financial effects could affect the value of the New Zealand dollar and place additional pressure on (already high) domestic inflation. It is these factors which could have the most significant flow on effects to the New Zealand economy.

Energy prices could rise, particularly for oil

With energy markets already reacting to the invasion, the biggest effect on New Zealand is the likely significant movement in global oil prices. Oil and gas markets could be significantly affected by economic sanctions, disruptions due to the invasion itself, or counter sanctions imposed by Russia itself.

Russia’s influence on the oil market is significant. It is the world’s second-largest exporter of crude oil after Saudi Arabia, producing around 10% of global supply and is a key member of the OPEC+ alliance.

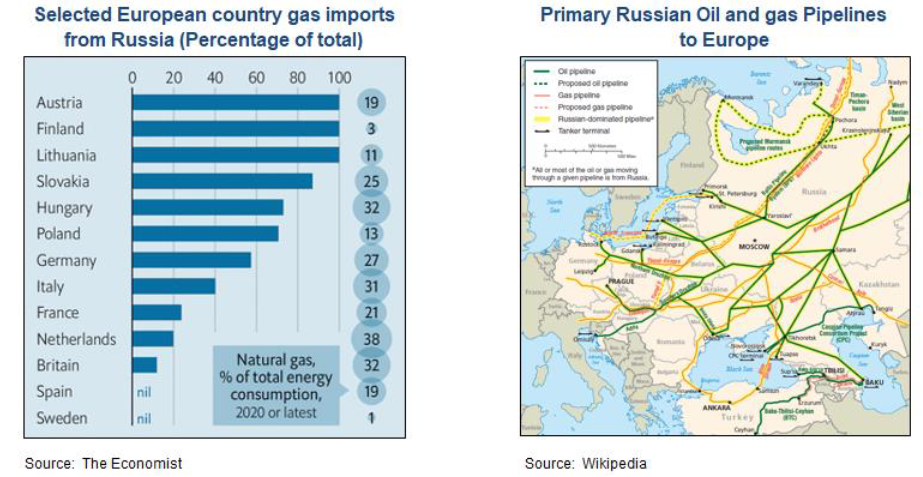

Ukraine moves Russian oil (11.9 million tonnes in 2021) to Slovakia, Hungary and the Czech Republic. In addition, about 35% of the EU’s natural-gas imports come from Russia. These mostly come through pipelines which cross Belarus and Poland to Germany. Nord Stream 1 goes directly to Germany via the Baltic Sea, while others pass through Ukraine itself.

Any disruption to Russian gas flows would lead to higher natural gas prices, and would ultimately increase demand for heating oil in Europe. With spare capacity so low, the oil market is currently highly vulnerable to supply disruptions in the short term.

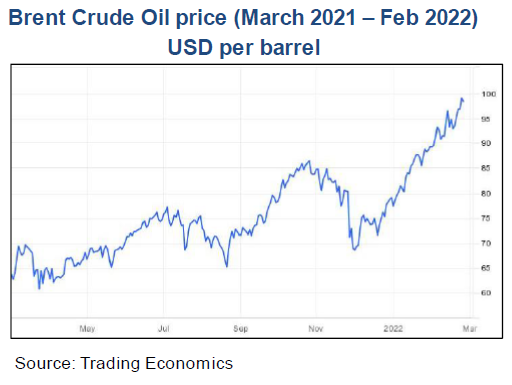

All this is occurring at a time when many members of OPEC and its allies (which include Russia) are struggling to meet their quotas for increased production, due to under investment and COVID-related complications. As a result, the fear of disruptions is a contributing factor toward rising prices. The Brent crude oil has risen rapidly since the beginning of December and at close to USD 100 per barrel is sitting at a seven-year high.

The impact of these higher energy prices are already flowing through to fuel costs for New Zealand consumers and businesses and could increase further. Brent Crude Oil price (March 2021 – Feb 2022) USD per barrel Source: Trading Economics

The pivotal role of energy in the global economy will also mean that price rises will spill over to other markets too, further increasing global freight costs and the price of many other imported goods for New Zealand. For example, expensive power has already caused some aluminium smelters to close in Europe with the potential that increases in gas prices could cause further reductions in supply. As a result, aluminium prices (of which Russia is a major player in the global market) have risen over 15% since the beginning of December.

In addition, increasing gas prices could also hit fertilizer production on the European continent—for which gas is used as both raw material and fuel.

Disruption to global wheat and grain markets could be significant

The indirect impact of an invasion on global grain prices could be even more significant. Russia is the world’s largest exporter of wheat, with Ukraine the fourth biggest. Ukraine is also the world’s third largest exporter of corn.

Together they export 28.6% of the world’s wheat and 19.6% of corn, with a significant proportion of Ukrainian cultivation taking place in its eastern regions, where much of the invasion is already taking place. Chicago Board of Trade Wheat Futures March 2021 – February 2022 (USD per Bushel) Source: Trading Economics

The nearby Black Sea also serves as a major conduit for international grain shipments. If there is damage to port infrastructure or disruption to shipments then this could have long-lasting impacts that could stretch into future crop seasons. Any interruption to the flow of grain out of Russia and Ukraine is likely to have a major impact on prices because the demand for wheat is so inelastic.

This is occurring at a time when falling grain stocks in America and Europe and bad weather in South America is already placing upward pressure on prices. As a result, Chicago wheat futures are trading 30% higher than they were a year ago. In addition to gas, Russia is a big producer of urea and potash, important ingredients for fertilizers used in the production of these crops.

Any disruption or export sanctions on these commodities could put further upward pressure on global grain and cereal prices, although the impact may be difficult to predict and will depend on the extent of the invasion. However when Russia annexed Crimea in 2014, concerns about the disruption of supplies from the Black Sea drove wheat prices up around 25% in two months.

This has implications for New Zealand as a net importer of grains and cereals. New Zealand imported $328 million of cereals in the year ended June 2021, of which the majority was wheat and maize. Although a relatively small import commodity, rising imported grain prices would indirectly raise the price of farm feed for New Zealand farmers. While New Zealand sources its farm feed from other nations (mainly Australia and South East Asia), any pressure on prices in the global market would also up prices from these suppliers as well. New Zealand’s largely pasture based dairy and meat production system will help New Zealand farmers fare better than our overseas grain-fed competitors.

As a staple food product in many developing countries, rising wheat prices could exacerbate food insecurity in many regions, with potential implications for stability in those countries.

The New Zealand dollar may weaken as investors move to safe haven currencies

The threat of war has already spilled over into developed markets, seeing a big fall in risk appetite in international financial markets even before the invasion began. The invasion will likely further impact market confidence, with investors likely to respond by continuing a retreat to more “safe-haven assets” such as the US dollar, the Swiss franc, and the Japanese yen. NZD / USD Exchange Rate (Feb 2021 – Feb 2022) Source: Trading Economics

These safe haven currencies have outperformed in recent weeks, with the New Zealand Dollar weakening against the US Dollar. Although much of that will have been driven by signals for monetary policy tightening by the US Federal Reserve.

A weakening New Zealand dollar will boost the competitiveness of New Zealand’s exports. However it will also increase the price of imported goods, pressuring profit margins for domestic businesses, and further fuelling domestic inflation.

Proposed sanctions for an extended period would weigh on global growth

As a small export-focused nation, perhaps the biggest medium term impact to New Zealand’s economy may come from any consequent dampening in economic growth across the world economy.

The sanctions announced so far and any further imposed on Russia could hit the Russian economy hard. However this effect alone will have little impact on global growth. The size of Russia’s economy is negligible, accounting for about 1.7% of the world’s gross domestic product.

Cutting off Russia would hurt many European countries, particularly Germany, which has significant trade with Moscow. Russia is the EU’s fifth largest trading partner with exports of USD 89.6 billion in the year ended December 2020 and imports of USD 98.6 billion.

In particular the pivotal role of energy in the global economy means any inevitable price rises will spill over to other markets and act as a drag on global economic growth. Global inflation which was expected to peak and decline later this year will be further pressured by these higher energy prices. In the context of tight household purchasing power, that could lower global recovery prospects, including that of many (if not all) of New Zealand’s key trading partners.

The Russian economy may be better placed to withstand sanctions this time around

The impact that the invasion and sanctions have on global markets will also be dependent on the period of time over which Russia has the ability to withstand the economic cost.

Sanctions imposed after the annexation of Crimea and the beginning of the Ukrainian annexation in 2014 acted as a significant drag on Russia’s economic growth in subsequent years. However, the Russian economy is now in a significantly better shape than it was in 2014.

In 2014, Russia had little foreign currency reserves and a big foreign debt. Since then Russia has built a significant cushion of reserves and has cut down its exposure to foreign creditors. Therefore, although insulating its economy fully will be impossible, the economic consequences of war may be survivable for Russia, at least in the short term. At 19.3% of GDP, Russia now has very low levels of Government debt by international standards, with the share in dollars falling steadily in recent years, currently sitting at 16%. In addition, only a fifth of Russia’s sovereign bonds are held by foreigners. Critically, according to the Russian central bank, its foreign cash reserves are currently USD 634.1 billion, representing a USD44.1 billion increase over the past year.

Restricting Russia’s access to the SWIFT system could be potentially more damaging however, particularly in the short term, as it would restrict its ability to execute its international financial transactions. For the nation, this could potentially trigger currency volatility and possibly cause large capital outflows. In recent years, Russia has developed a financial messaging system of its own to try to emulate SWIFT which could mitigate some of these effects. However it is highly unlikely to insulate the financial system effectively, as it is still a marginal system mostly used only by Russian banks.

More reports

View full list of market reports.

If you would like to request a topic for reporting please email exports@mfat.govt.nz

Sign up for email alerts

To get email alerts when new reports are published, go to our subscription page(external link)

Disclaimer

This information released in this report aligns with the provisions of the Official Information Act 1982. The opinions and analysis expressed in this report are the author’s own and do not necessarily reflect the views or official policy position of the New Zealand Government. The Ministry of Foreign Affairs and Trade and the New Zealand Government take no responsibility for the accuracy of this report.