Primary Products, Sustainability:

On this page

Summary

- The UK is a world leader in wind power, particularly offshore generation where it is second only to China in total installed capacity.

- Wind power sits at the heart of the UK’s transition to a net zero economy and it is complementary to other low-carbon technologies in which the UK is actively investing such as green hydrogen production and nuclear power. The UK wants to further grow the sector and is aiming to treble its offshore capacity in the next seven years.

- But the sector is facing challenges. The cost of wind farm development has risen spectacularly in recent years, leading to the failure of the offshore wind auction this September as developers declined to put forward bids. Challenges with grid infrastructure and the planning process further hindered the sector’s expansion.

- Challenges notwithstanding, the UK wind power sector presents potential business opportunities. The sector is almost certain to grow, and opportunities in peripheral sectors (transport, training, maintenance) will grow alongside it. There are also opportunities for New Zealand businesses, iwi, government agencies, and local authorities to learn from the UK’s offshore wind experience as we embark upon our own offshore wind journey, beginning in South Taranaki.

Report

Wind power in the United Kingdom

With access to Europe’s best wind resources, the United Kingdom has positioned itself as a world leader in wind power, particularly offshore generation.

The UK’s current installed wind generation capacity exceeds 28 gigawatts (GW). Of this, more than 13 GW is generated offshore – the second largest offshore generation capacity of any country, behind only China.[i] UK waters host more than 50 wind farms (either operating or under construction), these include the world’s two largest offshore wind farms (Hornsea 1 & 2) and the largest floating wind farm (Kincardine). The Crown Estate hosts a live map(external link) that details the current output of the UK’s offshore wind farms.

The Crown Estate owns the seabed on which offshore wind projects are developed, and it allocates leasing rights in a competitive process(external link). The development consenting process is handled through the UK Planning Inspectorate(external link) (~5 years), with procurement for construction and operation occurring via Contracts for Difference (CfD)(external link) auctions (~2 years), before construction (~3 years) begins. The rights to operate offshore transmission assets are allocated separately by the UK energy regulator Ofgem once the wind farm is constructed.

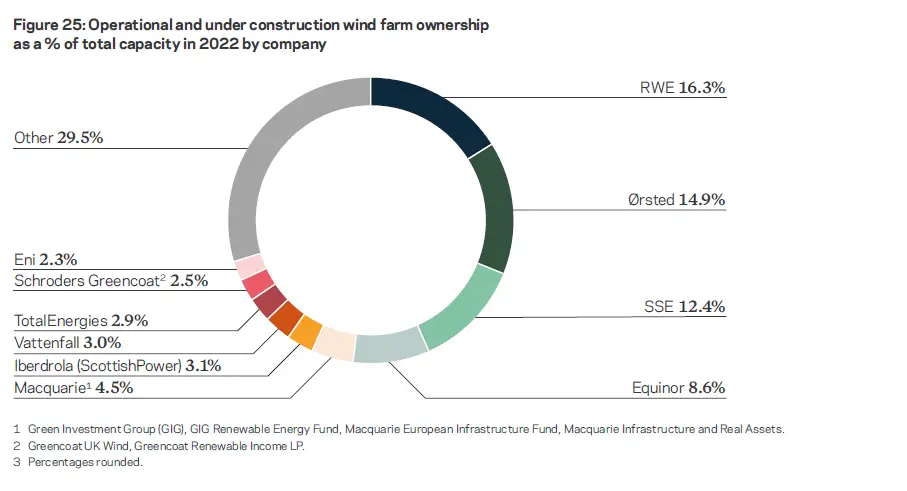

Four companies own over half of the UK’s offshore wind farms: German firm RWE, Danish energy giant Ørsted, UK-based firm SSE and Norway’s state-owned energy company Equinor (see graph in endnotes[ii]).

The role of wind power in the UK’s energy transition

The rapid scaling up of wind generation has been pivotal to the UK’s decarbonisation strategy. The UK’s wind generation capacity (both offshore and onshore) has increased fivefold since 2010. The UK intends to continue along this trend line with an ambitious target of trebling offshore generation by 2030.

The UK’s investment in wind is delivering results. In the past 12 months, roughly 30% of the UK’s electricity was produced by wind. In the first quarter of 2023 the UK passed a key renewable energy milestone, as wind overtook natural gas as the largest source of electricity generation (32.4% to 31.7% respectively) in a single quarter.[iii]

Wind energy is instrumental for growing the UK’s low-carbon hydrogen sector. The UK plans to utilise some of the output from wind farms to produce hydrogen via electrolysis and is establishing infrastructure clusters to co-locate the two low-carbon industries. It remains unclear how much of the UK’s wind generated power will be diverted to hydrogen production. The UK is aiming to produce 10GW of low-carbon hydrogen by 2030 – if this was all generated by wind power, it would use up roughly half of the UK’s planned offshore wind capacity according to one estimate(external link).

Challenges for the UK wind sector

It’s not all smooth sailing ahead. The sector is dealing with the rising cost of labour, materials and transport. The average cost for building a 1MW wind turbine is estimated to be 38% higher in 2023 than it was in 2021, and the average cost of necessary critical minerals is up 93% since 2020. The UK’s electricity grid infrastructure is also lagging behind the expansion of generators (primarily wind and solar) and industrial users that has occurred over the last decade. Strategic grid infrastructure now takes 12-14 years to be completed on average, and grid connection times have become prohibitively long with many projects being advised of 7-14 year waits. Both the governing Conservative Party and the opposition Labour Party have promised to reform the power grid in their 2024 election campaign platforms. Both parties’ approaches rely on increased centralisation, state involvement, and strategic prioritisation in the management of the grid – with Labour announcing their intent to set up publicly-owned energy company “GB Energy”; and the Conservative government pushing forward with a “spatial plan” to strategically coordinate energy infrastructure.

In September, the UK’s annual subsidies auction – which allocates contracts for new projects – failed to attract any offshore wind bids for the first time. Developers argued that the fixed energy prices set by the government via the auction process did not take into account the rising development costs outlined above. Statements from UK Government officials indicate that this price may be adjusted up for the next auction in March 2024. Onshore wind (and other renewables) projects were awarded contracts in the auction.

Onshore wind power has faced some additional challenges. Development of onshore wind projects in England slowed significantly from 2015 as the consenting process was changed to allow local objection to permanently freeze the construction of new wind farms – widely viewed as a de-facto ban. In September, the UK Government announced they would soften the language around community objections in the planning rules, but it remains unclear whether this will reinvigorate the onshore wind sector. Onshore wind development has continued apace in Scotland, where different rules apply.

International collaboration

The UK collaborates with its European neighbours on offshore wind. As part of the North Seas Energy Cooperation (NSEC) grouping, the UK collaborates with seven EU member-states and Norway to build and expand an offshore energy grid linking offshore wind farms and transmission infrastructure to the UK and continental energy grids. In April, the Netherlands and the UK announced plans for a novel electricity link (dubbed ‘Lion Link’) between the two countries, via a large Dutch wind farm.

Opportunities for New Zealand

New Zealand is aspiring to meet all of its electricity generation requirements through renewable production by 2030 (~85% of New Zealand’s electricity is currently generated from renewable sources). New Zealand has already established a sizeable onshore wind generation capacity (~10% of installed generation capacity), but until now has not commercially developed its offshore wind assets. New Zealand’s first commercial offshore wind farm(external link) is currently being planned off the coast of southern Taranaki, and the New Zealand Super Fund has partnered with Copenhagen Infrastructure Partners on a joint project(external link) to accelerate offshore wind development in the area. Offshore wind projects are also being explored off the coast of Waikato and Murihiku-Southland. As our offshore wind sector expands, New Zealand businesses, councils, iwi and Government bodies may look to learn lessons from the UK’s experiences.

The growth of the UK wind sector could also present opportunities for New Zealand businesses and iwi. While offshore wind farm construction and operation is on a scale that limits New Zealand business involvement, there will be opportunities in the peripheral sectors, including training, maintenance, personnel and equipment transport, and onshore services (i.e. accommodation and hospitality) that New Zealand businesses could explore. There may also be new opportunities in the UK’s onshore wind generation sector if the planning process becomes less restrictive.

External links

The following links may provide useful information to businesses:

[i] https://www.renewableuk.com/page/UKWEDhome(external link)

[ii] https://www.thecrownestate.co.uk/en-gb/what-we-do/on-the-seabed/energy/offshore-wind-report-2022/(external link)

[iii] https://www.cnbc.com/2023/05/12/wind-power-was-britains-largest-electricity-source-in-first-quarter.html(external link)

More reports

View full list of market reports(external link)

If you would like to request a topic for reporting please email exports@mfat.net

Sign up for email alerts

To get email alerts when new reports are published, go to our subscription page(external link)

Learn more about exporting to this market

New Zealand Trade & Enterprise’s comprehensive market guides(external link) cover export regulations, business culture, market-entry strategies and more.

Disclaimer

This information released in this report aligns with the provisions of the Official Information Act 1982. The opinions and analysis expressed in this report are the author’s own and do not necessarily reflect the views or official policy position of the New Zealand Government. The Ministry of Foreign Affairs and Trade and the New Zealand Government take no responsibility for the accuracy of this report.