Supply Chains, Food and Beverage, Primary Products:

On this page

Summary

- The United States (US) and Israel conflict with Iran represents a key risk to the global economy and New Zealand’s trade into the region.

- At $3.4bn, New Zealand’s total exports to the Persian Gulf region represent just 3.0 percent of our total exports. However, these exports are highly concentrated and dominated by dairy products into the UAE and Saudi Arabia, which are key markets for whole milk powder and butter.

- The region is also a key source for fertilisers, representing 22 percent of New Zealand’s fertiliser imports.

- Of most concern for the New Zealand economy is the potential for a protracted period of disruption to global energy supply, particularly the disruption to oil transiting the Strait of Hormuz.

- While New Zealand no longer imports crude oil from the Gulf region, countries in Asia from which we now import refined product have high dependencies on the Middle East for their oil supplies.

- Disruption to this critical supply chain will lead to elevated prices for fuel and could bring broader inflationary pressures to the global economy, including to New Zealand.

- The conflict may also lead to increased volatility to global financial markets, increasing the risk of asset market volatility, increased risk premiums for borrowing costs, and a weaker New Zealand dollar.

- To date markets have remained relatively calm. Oil prices have increased significantly, but are well below levels experienced in the aftermath of Russia’s invasion of Ukraine. Similarly, equity markets and the New Zealand dollar have shown some recent softening but have remained relatively stable, despite the uncertainty being caused by the conflict.

- In addition to global supply chain disruption, events in the Middle East are also likely to add to geopolitical uncertainty, which may further weigh on global growth. In turn, weak global growth would be expected to reduce overall demand for New Zealand’s exports.

Report

On 28 February 2026, the United States and Israel launched coordinated large-scale strikes inside Iran. Iran subsequently responded within hours with waves of ballistic missiles and drones, aimed not only at Israel and US forces but also at Gulf states hosting US bases, including Saudi Arabia, Qatar, Bahrain, Kuwait, and the United Arab Emirates (UAE).

At present, despite Iran announcing the closure of the Strait of Hormuz, vessel tracking has indicated reduced movement but not a complete shutdown. With it being one of the world’s most critical oil corridors, oil prices and shipping traffic through the Strait are strongly linked. Across the wider region, most Gulf and Middle Eastern airspace is still closed or heavily restricted. Dubai, Abu Dhabi, and Doha airports are operating only limited flights, and flights across the region are still suspended or severely disrupted.

Our bilateral trade with the Middle East is relatively small but concentrated

A key channel through which events in the Middle East are likely to impact the New Zealand economy is via the potential disruption to global supply chains and trade. At $3.4 billion, New Zealand’s exports to Middle Eastern countries for the year ending December 2025 represented just 3.0 percent of our total exports. Similarly, a minor 0.6 percent ($642 million) of New Zealand’s total imports are sourced from Middle Eastern countries.

However, New Zealand’s trade in the region faces some notable short-term exposure.

New Zealand’s exports to the region are, however, highly concentrated by product and destination. For instance, dairy products ($2.3bn) represent almost 70 percent of New Zealand’s exports to the region. Similarly, 85 percent of New Zealand’s exports to the region are destined for Saudi Arabia ($1.45 bn) and the UAE ($1.46bn) (see Table 1).

Table 1: Export value to the Middle East Region in 2025

| Export Goods ($ million) |

Export Services ($ million) |

Total Exports ($ million) |

Percentage of global exports | |

|---|---|---|---|---|

| Middle east region | 3,325 | 91 | 3,416 | 3.0% |

| United Arab Emirates | 1,463 | * | 1,463 | 1.3% |

| Saudi Arabia | 1,426 | 20 | 1,446 | 1.3% |

| Oman | 147 | 8 | 155 | 0.1% |

| Kuwait | 131 | 22 | 153 | 0.1% |

| Bahrain | 93 | 2 | 96 | 0.1% |

| Qatar | 51 | 11 | 62 | 0.1% |

| Iraq | 12 | 0 | 12 | 0.0% |

| Iran | 1 | 28 | 29 | 0.0% |

Notes: * missing data may be due to data suppression for reasons of confidentiality.

Whole milk powder ($1.2 bn) and butter, fat, and cream products ($617m) are among our most exposed export goods representing 13.2 percent and 10.2 percent of global exports for these products (see Table 2 below). Given these concentrations, dairy exporters may face some short-term challenges to quickly redirect trade to other markets.

Table 2: Top 10 goods exports to the Middle East Region by value in 2025

| Industry Product |

Export Value ($ million) |

Exports to the Middle East as a proportion of global exports |

|---|---|---|

| Dairy | 2,429 | 8.4% |

| Whole milk powder | 1,208 | 13.2% |

| Butter, fat & cream | 617 | 10.2% |

| Cheese | 168 | 4.9% |

| Skim Milk & Butter Milk Powder | 165 | 7.3% |

| Other dairy products | 136 | 5.4% |

| Casein & Protein Products | 127 | 4.0% |

| Meat | 331 | 2.6% |

| Sheep meat | 147 | 3.1% |

| Beef meat | 125 | 2.5% |

| Other animal products | 59 | 1.8% |

| Industrial | 281 | 2.1% |

| Machinery & Equipment | 220 | 4.0% |

While travel services represent around 90 percent of all service exports to the Middle East, this represents a very small proportion (0.7 percent) of New Zealand’s total travel exports.

Service imports from the Middle East represent a very minor 5.0 percent ($32 million) of New Zealand’s total imports from the Middle East. However, these imports are also highly concentrated with just over 70 percent of Middle Eastern imports coming from Saudi Arabia and the UAE.

Imported fertiliser is our most exposed imported good with over a fifth of our global supply coming from Saudi Arabia. (Table 3). However, Ministry of Primary Industries (MPI) advise that domestic supplies are sufficient to cover the upcoming Autumn application for farmers. Other import goods of note include aluminium (8.8 percent of total imports), jewellery (7.2 percent) and minerals (5.9 percent).

Table 3: Top 10 goods imports from the Middle East by value in 2025

| Industry Product |

Import Value ($ million) |

Imports from the Middle East as a proportion of total imports |

|---|---|---|

| Primary products | 294 | 2.1% |

| Fertilisers | 236 | 21.7% |

| Other Primary Products | 37 | 1.0% |

| Other Animal Products | 8 | 1.0% |

| Industrial | 269 | 0.6% |

| Plastics | 90 | 4.1% |

| Fuel | 60 | 0.6% |

| Aluminium | 54 | 8.8% |

| Other | 19 | 0.3% |

| Minerals | 18 | 5.9% |

| Iron & Steel | 9 | 0.6% |

| Consumer | 42 | 0.3% |

| Jewellery | 39 | 7.2% |

Beyond our direct trading relationship, the Persian Gulf, particularly the UAE and Qatar, also plays an important role for New Zealand trade as a global hub for the transshipment of goods and the transport of people further afield. For New Zealand, Dubai international airport is an especially important transit hub for high-value low volume exports and imports to and from Europe.

In the short term, the closure of several airports in the region may also increase the risk of disruption to the export of some perishable products, and some high value imports sourced from Europe – such as pharmaceutical products. Moreover, New Zealand’s service exports, such as tourist arrivals from Europe, are likely to face short-term disruptions with airspace closed or under emergency restrictions over much of the Middle East at present.

Despite the immediate impacts, we expect most supply chains affecting New Zealand trade to reconfigure if this conflict becomes protracted, ameliorating some of the short-term disruptions currently being experienced. Vessel rerouting is already occurring via alternative corridors, including around the Cape of Good Hope, albeit affecting transit times and operational costs.

Disruptions to shipping in the region are impacting prices for energy commodities

Of more concern for the New Zealand economy is the disruption to energy markets, with the Middle East being a major source of global oil and gas supply. Moreover, the Strait of Hormuz, at the entrance of the Persian Gulf, is a crucial transit route for global energy trade from major oil and gas fields in the region to markets abroad, with around 20 percent of global oil supply transiting this waterway.

There are limited alternatives to divert oil from Persian Gulf countries, with pipelines in Saudi Arabia, the UAE, and Oman only able to shift a fraction of the oil that typically transits the Strait. In addition, there are also reports of Iranian attacks on oil and gas infrastructure in the region which poses further risks to global energy supplies. While this disruption continues this is likely to have spillover effects on global energy prices.

International energy markets were already nervous ahead of the hostilities over the weekend. Brent crude futures had risen by over USD12 a barrel from a low point of USD60 at the beginning of the year as traders tracked various global geopolitical risks, including in the Middle East. Since the conflict began prices have risen a further USD10 to over USD83 per barrel, as mounting risks of a full shutdown of the Strait of Hormuz are increasingly factored into global supply chains.

Similarly, European natural gas futures have surged by over 50 percent as QatarEnergy suspended the production of liquified natural gas in its Ras Laffan and Mesaieed complexes, responsible for around 20 percent of global LNG supply, following a drone attack at the energy facility. The suspension of supply from Qatar threatens around 15 percent of LNG imports to the European Union and the UK, magnifying the risks to an already tight global LNG market.

While there are significant global stockpiles of oil (if needed) at present, the capacity to replace oil supply from the Persian Gulf as stockpiles are drawn down is limited (see Figure 1). OPEC has already announced a desire to increase output, with eight oil-producing countries—including Russia, Saudi Arabia and several Gulf States announcing that they will increase oil output by 206,000 barrels a day in April. However, some of these countries are limited in their ability to get product to market while shipping is disrupted in the Gulf.

Figure 1: OPEC spare capacity

Should the release of spare capacity be held back in the case of disruption to oil flowing through the Strait of Hormuz, coordinated releases from the strategic petroleum reserves by the International Energy Agency may also help stabilise prices. Alternatively, over the medium term, higher prices could incentivise higher cost producers, such as US shale producers, to lift their production.

For now, there is significant uncertainty regarding the extent to which global oil prices will respond over the medium term. Some analysis suggests that global oil prices could almost double compared to January lows to exceed USD100 per barrel in the event of a complete closure of the Strait of Hormuz.

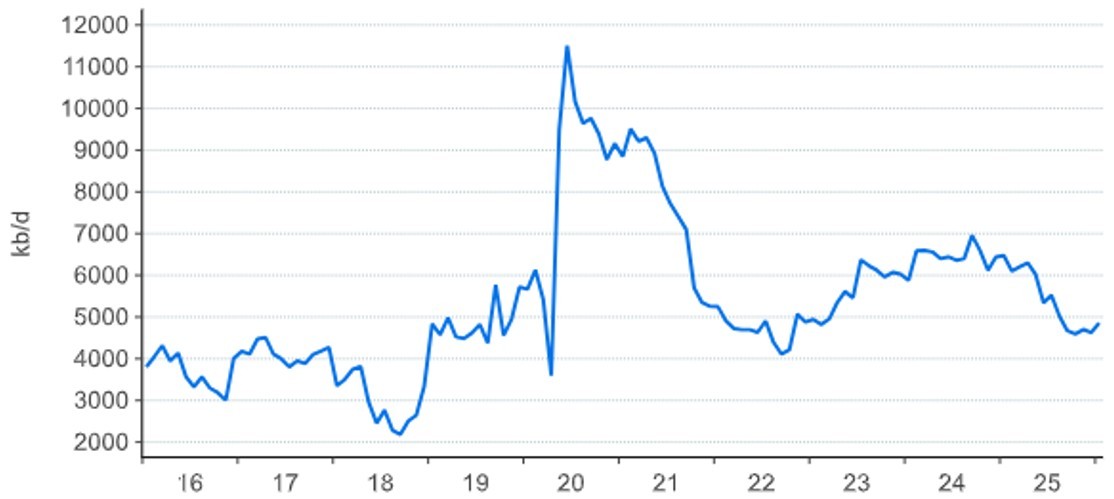

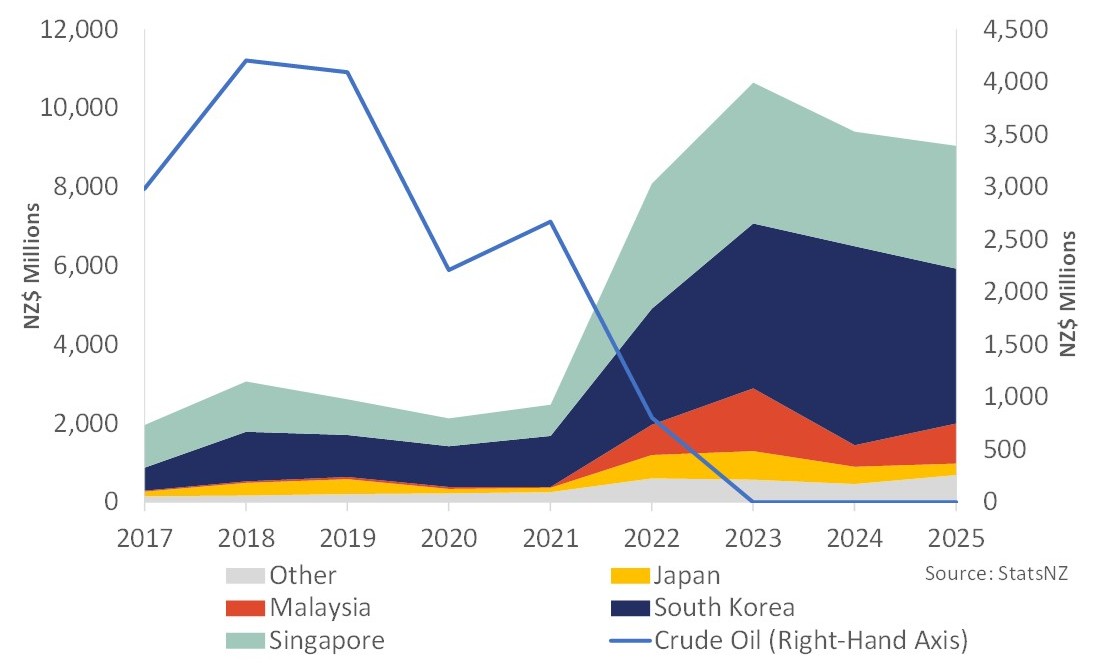

Despite no longer importing crude oil, New Zealand still faces significant second-order exposure to global oil markets

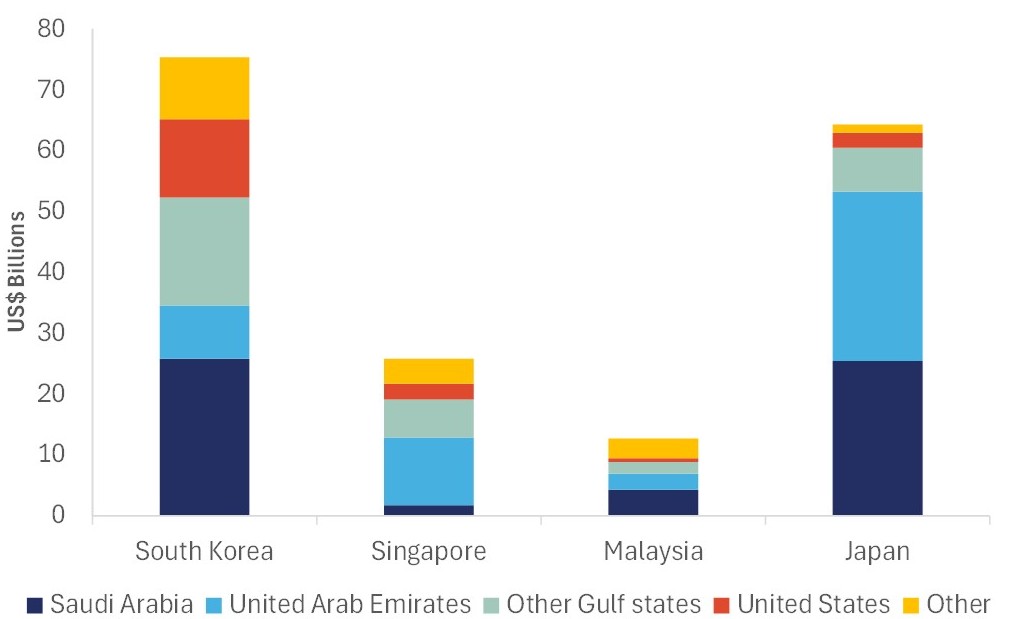

With the transition of the Marsden Point oil refinery to a refined product import terminal in 2022, New Zealand no longer imports crude oil (see Figure 2a below). Over the last five years, New Zealand has sourced over 90 percent of petroleum imports from a handful of Asian economies that include South Korea (45 percent), Singapore (34 percent), Malaysia (8.4 percent), and Japan (5.3 percent). Over the same period these four economies have sourced just over three quarters of their crude oil imports from countries bordering on the Persian Gulf (see Figure 2b below).

Figure 2a: New Zealand’s petroleum product imports by main trading partner

Figure 2b: South Korea, Singapore, Malaysia, and Japan crude oil imports by trading partner in 2025

If supply from the Persian Gulf is disrupted then these Asian refineries will be forced to compete for oil supply from elsewhere, putting upward pressure on global oil prices, with consequences for imported petroleum products into New Zealand.

An extended period of rising fuel costs would likely be a drag on household consumption at a time of ongoing cost of living pressures. Rising oil prices won’t just show up at the petrol pump but will also pervade the economy via rising business costs for services such as transportation and energy intensive goods such as fertilisers.

Increased economic uncertainty may also impact global financial markets

The conflict may also bring increased volatility to global financial markets, driven by heightened global uncertainty. Any increase in risk premiums for non-safe haven assets may weigh on global equity markets and add risk premiums to global interest rates.

As of 5 March, market responses have been relatively measured, albeit with increased risk sentiment and risks to global growth weighing on markets. As of 4 March, Japan’s Nikkei had fallen 7.8 percent, while the Euro Stoxx 600 index has fallen by 4.6 percent since the conflict began. The US S&P500 initially fell as much as 2.5 percent on 4 March before recovering to be down 1.4 percent since 27 February’s close. New Zealand’s NZX50 has shed 0.6 percent since the conflict began.

The USD has strengthened considerably over the week (appreciating by over 1.0 percent against partner currencies) helped by its safe-haven status and position as a net exporter of oil and gas. By contrast, the increasing global risk sentiment has weighed on the New Zealand dollar which was down by as much as 2.1% on 3 March since the conflict began but had partially recovered on 4 March to be down around 1% since the start of the week. A sustained weakness in the New Zealand dollar will support exporter profitability over the medium term. However, a weaker dollar would be expected to add upward pressure to the costs of imported goods.

Over the medium term, a sustained period of high oil prices and elevated uncertainty could also weigh on global economic growth

A sustained period of high oil prices and economic uncertainty is likely to weigh on global economic growth over the medium term. While the magnitude of potential economic impact is still uncertain, lower global growth will have implications for many of New Zealand’s key export markets. Like New Zealand, many trading partners are net oil importers and would face similar inflationary pressure and slowing economic activity. Rising energy prices will also weigh on New Zealand’s trading partner growth, which would reduce demand for New Zealand’s exports. Domestically this elevated global uncertainty is also likely to weigh on New Zealand business investment and household spending.

Of those, Asia is likely to be disproportionately impacted, as most oil traffic from the Gulf is destined for Asian markets. Markets such as India and Indonesia, which rely heavily on Middle Eastern oil, could be more vulnerable. By contrast, China (where nearly 90 percent of Iran’s oil exports go) has relatively diversified oil import sources and significant reserves. While Europe’s demand for LNG has increased since the Russia-Ukraine conflict, its reliance on the Middle East has fallen with increased imports from the US in recent years. Nevertheless, many European economies remain highly sensitive to rising energy prices.

Ultimately, the magnitude of the impact on the New Zealand economy will depend on how the conflict unfolds from here

If the conflict remains largely contained between the current three actors and should disruption of trade flows through the Strait of Hormuz be short lived, the worst of the economic impacts are likely to be contained to key sectors via short-term supply chain disruptions. However, should the conflict broaden regionally, with other actors entering the theatre, or extend for a prolonged period, particularly with a full closure of shipping through the Strait, then the medium-term risks to our trade and economic interests are likely to be more significant.

More reports

View full list of market reports

If you would like to request a topic for reporting please email exports@mfat.govt.nz

Sign up for email alerts

To get email alerts when new reports are published, go to our subscription page(external link)

Learn more about exporting to this market

New Zealand Trade & Enterprise’s comprehensive market guides(external link) export regulations, business culture, market-entry strategies and more.

Disclaimer

This information released in this report aligns with the provisions of the Official Information Act 1982. The opinions and analysis expressed in this report are the author’s own and do not necessarily reflect the views or official policy position of the New Zealand Government. The Ministry of Foreign Affairs and Trade and the New Zealand Government take no responsibility for the accuracy of this report.

Copyright

Crown copyright ©. Website copyright statement is licensed under the Creative Commons Attribution 4.0 International licence(external link). In essence, you are free to copy, distribute and adapt the work, as long as you attribute the work to the Crown and abide by the other licence terms.