Supply Chains:

On this page

Prepared by the Economic Division in Wellington

Rāpopoto - Summary

- Given the ongoing risks to New Zealand’s global supply chain connections since the COVID-19 pandemic, MFAT’s network of Posts and the Trade Recovery Unit have been monitoring the operations of New Zealand’s sea and air freight connectivity, and have published reports on this since June 2020. This report provides a snapshot of how global supply chains are functioning offshore, significant international initiatives affecting supply chains, and other issues of interest to New Zealand exporters and importers.

- To provide feedback or information relevant to this report – please contact exports@mfat.net.

Pūrongo - Report

Waka rererangi – Air freight

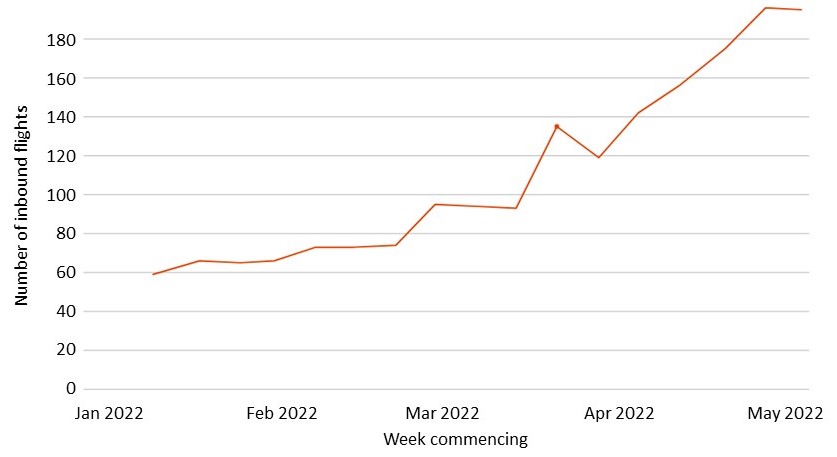

- Air connectivity is improving following New Zealand’s border reopening to Australians on 12 April and visa waiver tourists on 1 May (with full reopening to all visa categories by 31 July).

- The frequency of flights to and from New Zealand has increased over the quarter. Up to 50 flights per day are scheduled to arrive in Queenstown in July, which is close to 2019 levels of 60 flights per day during the peak winter ski season. Auckland Airport currently has 18 airlines flying to 33 destinations – about 48% of 2019 capacity.

- A range of international airlines have either resumed flying or confirmed dates to resume flying to New Zealand. These include Air Tahiti Nui in May, Cathay Pacific in June, and Hawaiian Airlines in July. Some airlines have announced brand new routes, such as Air New Zealand flying direct from Auckland to New York in September. American Airlines will be operating daily, non-stop flights between Auckland and Dallas, Texas from October. This could improve airfreight capacity and frequency of flights to the North American market.

- However, global labour shortages and high jet fuel prices are hampering recovery. Airports are having difficulty attracting specialised skills such as ground handling staff; and retail, food and beverage options remain limited. Some airlines are seeing a high attrition rate, particularly among cabin crew. According to Hawaiian Airlines(external link), April 2022 prices for jet fuel were 137% higher than April 2021, and price volatility makes long-term planning difficult.

- Full recovery of the aviation industry is likely to be a few years away. Oxford Economics, an international economic consultancy, forecasts that global passenger volumes will reach 72% of 2019 levels by the end of 2022, and 94% by 2025. Air New Zealand similarly anticipates(external link) that it will reach 75% of its pre-COVID international capacity by December 2022.

Number of direct inbound passenger flights to New Zealand

Mārunga moana – Sea freight

- International sea freight remains subject to delays and congestion, constrained capacity, and elevated prices.

- Shipping delays reached record highs in April. According to Flexport’s Ocean Timeliness Indicator(external link), the time taken for containers to travel across the Far East Westbound route (China to Europe) topped 120 days for the first time ever. Times taken for the Transpacific Eastbound route (China to the US) peaked at 110 days. Flexport attributes the deterioration to port congestion in Shanghai combined with seasonality.

- As bottlenecks in Asia have eased, shipping delays have been somewhat alleviated. The time taken for containers to travel across the Transpacific Eastbound route was down to 97 days and the Far East Westbound route was 95 days at the end of June. Yet these figures remain well above pre-pandemic levels. Travel times were under 60 days for both routes in June 2019.

- Lack of labour and ships are hindering global capacity. Drewry, an independent maritime research consultancy, projects that there will not be enough ocean-ready ships built to meet demand until 2024.

- Prices are going up for ships to transit through major waterways. In May, the Suez Canal Authority increased tariffs by 5-10% for ships travelling through the Suez Canal. The Panama Canal Authority is likewise considering a new toll structure(external link) that could see costs gradually increase from 2023-2025.

95 days for containers to travel from China to Europe

97 days for containers to travel from Europe to China

Regional Updates

China

- Shanghai’s Omicron outbreak and associated lockdown exacerbated global supply chain disruption this past quarter. As home to the world’s largest container port and a major airport, some flow-on supply chain effects persist following the lockdown ending on 1 June.

- The Port of Shanghai experienced significant delays and congestion during the lockdown. At the height of the outbreak, international analysts estimated that the port was operating at a third of normal capacity due to warehousing shortages and workforce absences. Refrigerated storage capacity was particularly affected, with Maersk temporarily suspending bookings for reefer (refrigerated) cargo ships as storage facilities in Shanghai were full. While waiting times for container ships to berth reached 69 hours in April, they are now at 31 hours – which is only four hours above the port’s three-year average.

- Trucking capacity in and around Shanghai was also limited under lockdown conditions. Operations temporarily dropped to around 15% of normal levels, and road haulage prices rose several fold. Chinese leaders responded by announcing(external link) one trillion RMB to mitigate bottlenecks across the country, and the State Council issued guidelines(external link) to minimise disruptions to vehicle freight. In the period since the lockdown, at least 80% of truck drivers are now able to work (versus 50% in April).

- Operations at Shanghai’s Pudong Airport were affected by staffing shortages at the peak of the outbreak. Flexport recorded that over 80% of commercial freighter services to and from this airport were cancelled in April. This resulted in Air New Zealand pausing passenger flights to and from Shanghai during the second half of May, as well as the sporadic cancellation of flights operated by China Eastern Airlines. Air New Zealand was able to maintain its cargo flights during most of this period (currently at six cargo flights per week), and its passenger flights have now resumed.

- Some Shanghai-based manufacturers were permitted to operate during the lockdown on the condition of a ‘closed loop’ model, where employees lived onsite in a single ‘bubble.’ However, not all manufacturers had suitable accommodation, and production levels dropped for some goods.

- Demand for New Zealand products in China generally remained strong through this challenging period. Some large New Zealand exporters were able to adapt by redirecting shipments to other Chinese ports, diverting product to different markets, or changing the type of product sent (e.g. frozen meat instead of chilled or fresh). Group buying, having gained prominence during the lockdown as one of the few reliable methods for purchasing essentials, has been a trend that presented opportunities for New Zealand food and beverage (e.g. kiwifruit, apples, pumpkins and avocadoes).

- It may be too early to tell the full impact of these events on New Zealand exporters. The Centre for Strategic and International Studies notes(external link) that COVID outbreaks will continue to trigger the imposition of lockdowns in China, so it may be some time before the financial implications become clear.

Sri Lanka

- Sri Lanka is experiencing shortages of fuel, gas, medicines and food as the result of a political crisis. Food inflation for June reached 80% (the highest figure ever recorded), and restrictions were placed on non-essential goods. The majority of goods imported from New Zealand are exempt as they are considered essential. Shipping companies are rerouting to Indian ports instead of going through Colombo.

South Korea

- There are shipping delays at Busan port. Over 25,000 truck drivers went on strike in June, demanding freight rates that would guarantee basic wages. Although an agreement was reached after one week, the strike caused a backlog of containers to build up at the port. The length of dwell time increased from 3-4 days to 14 days and may take a while to subside.

- South Korea has adopted an early warning system to safeguard access to critical and essential goods. It is tracking 4000+ items where there is more than 50% dependency on a single market source, with items categorised from A-D depending on their significance.

Ukraine

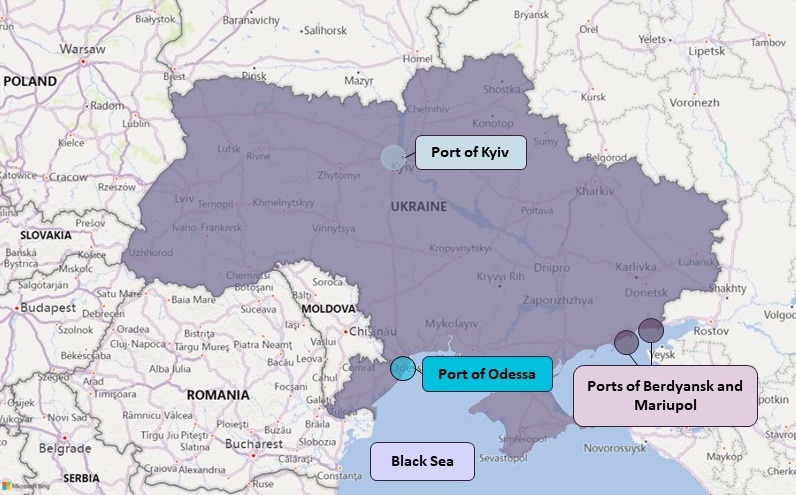

- Russia’s invasion of Ukraine, and the resulting economic sanctions and Russia’s retaliatory sanctions, continue to heighten supply chain issues globally.

- International sea freight from Ukraine is experiencing delays since there are no functioning ports in Ukraine as a result of Russia’s blockade of the Black Sea (see map below). Ports in Romania, such as Constanta, are operating at maximum capacity. Shipping through the northern Baltic ports is also difficult as this requires transiting through either Poland or Belarus. With Belarus refusing to allow transits of goods unless sanctions are lifted, Poland is the only option available.

- Cargo is being diverted to road and rail as a result of shipping disruption. However, this presents logistical challenges because of a railway gauge difference between Ukrainian and European railway systems. There are also shortages of truck drivers in Ukraine, as working-age (16-60) men are banned from leaving Ukraine. Shipping costs in the region have consequently increased by 50-80% since the start of the war, and insurance premiums charged on ships in or around the war zone are up by 500%.

- The conflict is also affecting global container supply. Shipping containers located in Russia cannot be moved easily due to sanctions. Maersk has established a pop-up container yard in Kalundborg, Denmark to store containers that were originally destined for Russia, but require rerouting. The terminal held more than 8000 containers in April, while Maersk’s customers gradually resold goods and shipped them to different markets.

- New Zealand is impacted through increased energy, food and commodity prices. World gas prices have risen by 70%, oil by 19% and food by 13% since the beginning of invasion.

- Russia is preventing over NZ$14 billion worth of grain being exported by Ukraine. In response to food shortages, some countries are restricting exports of foodstuffs to safeguard domestic prices. For example, India has limited exports of wheat and sugar, and Malaysia has done the same with chickens.

United States

- Shipping congestion at the twin ports of Los Angeles and Long Beach is improving. The number of vessels waiting to berth dropped from 109 in January, to about 50 in March, to 19 in May. But there have been fewer ships arriving from Asia, and a surge may be possible as Shanghai reopens.

- The US is grappling with an infant formula shortage. In February, a large manufacturer of powdered infant formula closed a facility and issued a voluntary recall following contamination. Supply dropped below 50% of normal levels in some states. President Biden invoked the Defence Production Act to boost domestic production, and ordered the Pentagon to procure supply from overseas, including from New Zealand. Danone New Zealand, a French food group with formula-making facilities in New Zealand, has been given approval by the Federal Drug Administration to contribute 550,000 cans from New Zealand.

- The US Government is investing in new initiatives to counter global shipping problems. President Biden signed the Ocean Shipping Reform Act in June, which gives the Federal Maritime Commission (FMC) more authority to regulate ocean carrier practices. Additionally, the Act prohibits carriers from unreasonably refusing cargo space or charging excessive fees.

- The FMC completed a two-year investigation into potential anti-competitive behaviour in the shipping industry. Its final report(external link) of 29 May concluded that high ocean freight rates have been determined by “unprecedented consumer demand” rather than anti-competitive behaviour.

South Africa

- Flooding caused substantial damage to South Africa’s roads, railways and bridges in April. The Port of Durban, which is the country’s largest port and a primary gateway for goods into southern Africa, was briefly closed. This left a backlog of 8000-9000 containers to be cleared, and there were media reports of theft from containers that washed out of the shipping yard onto the freeway.

Supply chain resilience initiatives

- New Zealand is part of a group of fourteen Indo-Pacific economies working to develop a US-led Indo-Pacific Economic Framework for Prosperity (IPEF). A Joint Statement(external link) released on 23 May provides an overview of the initiative, which is “intended to advance resilience, sustainability, inclusiveness, economic growth, fairness, and competitiveness” for the region’s economies. One of the four pillars of IPEF focuses exclusively on supply chains, with a view to “improving transparency, diversity, security, and sustainability in our supply chains to make them more resilient and well-integrated.”

- Prime Ministers Jacinda Ardern and Lee Hsien Loong announced(external link) the establishment of a New Zealand-Singapore Supply Chain Working Group in April. Potential areas for supply chain collaboration include improving freight data, exploring how automation could help businesses to withstand supply chain disruptions, and sharing best practices for managing supply chain risks.

More reports

View full list of market reports.

If you would like to request a topic for reporting please email exports@mfat.net

Sign up for email alerts

To get email alerts when new reports are published, go to our subscription page(external link).

Disclaimer

This information released in this report aligns with the provisions of the Official Information Act 1982. The opinions and analysis expressed in this report are the author’s own and do not necessarily reflect the views or official policy position of the New Zealand Government. The Ministry of Foreign Affairs and Trade and the New Zealand Government take no responsibility for the accuracy of this report.